AXON Q4 2024 Earnings: Deep Dive into a Public Safety Powerhouse

$AXON

I've been talking a lot about Axon lately—mainly because its 30% drop in three days made no sense. It got swept up in the retail-driven selloff alongside Palantir, Robinhood, and Hims & Hers. But earnings dropped yesterday, and I think they crushed it. I am using the new ChatGPT deep research tool for this analysis - I am very happy with the outcome.

Axon Enterprise (NASDAQ: AXON) closed out 2024 with a bang – delivering another quarter of 30%+ growth and showcasing the fruits of its transformation from a TASER stun-gun maker into a full-fledged public safety technology platform.

1. Financial Deep Dive

Blistering Growth with Shifting Revenue Mix: 2024 marked Axon’s third consecutive year of 30%+ revenue growth, with full-year revenue up 33% to $2.1 billion. In Q4 alone, revenue hit a record $575 million (+34% YoY). Notably, Axon’s revenue is now evenly split between hardware and software:

TASER devices contributed approximately $819 million (around 39% of 2024 revenue, +~30% YoY) – fueled by surging demand for the new TASER 10.

Axon Cloud & Services (software subscriptions) delivered $806 million (~39% of revenue, +44% YoY). This segment’s rapid growth highlights Axon’s evolution into a software-centric business.

Sensors & Other (body cameras, in-car video, etc.) made up roughly $458 million (~22% of revenue, +18% YoY), showing solid growth but a smaller share of the pie.

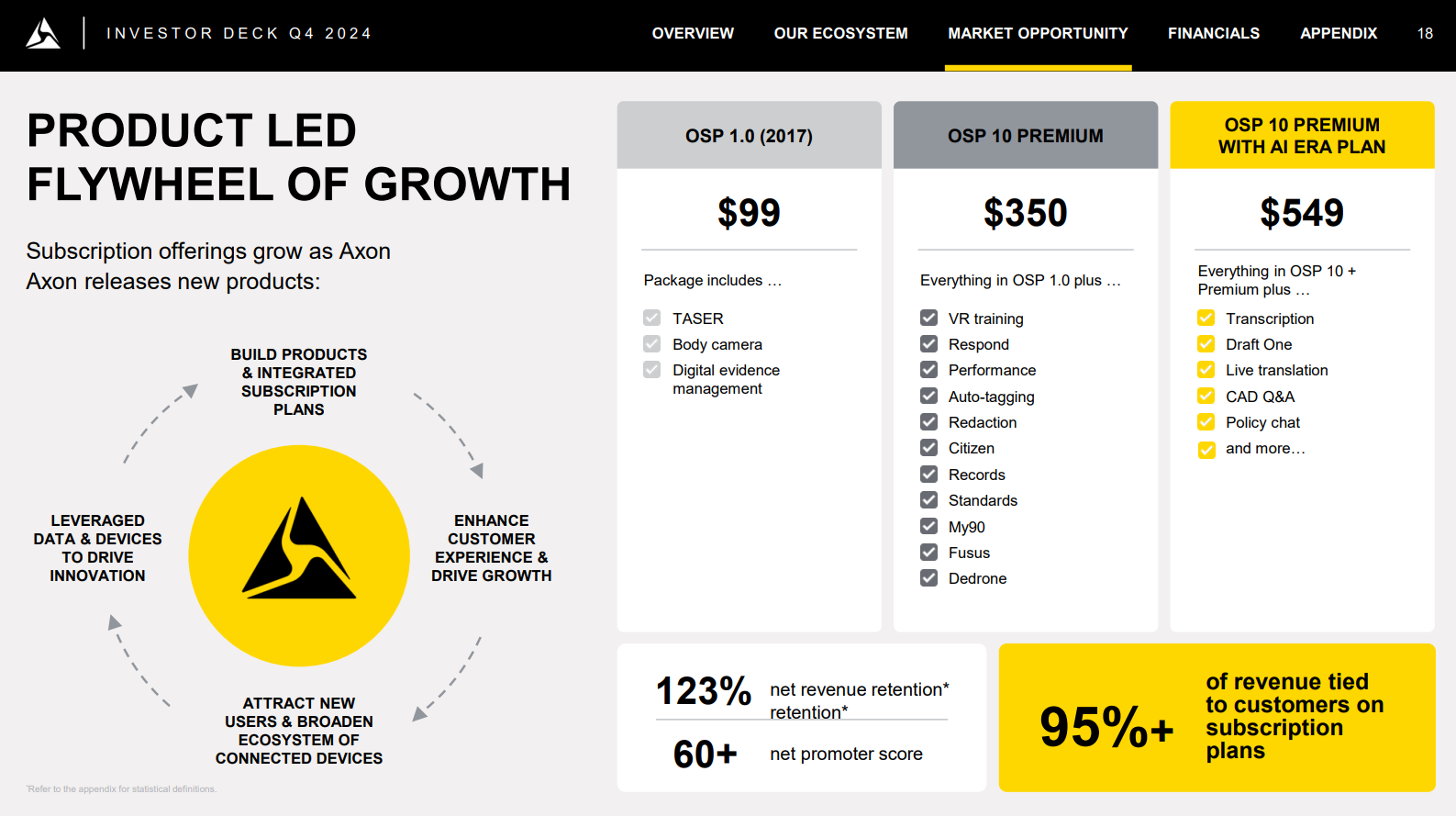

In Q4, Axon Cloud & Services accounted for 40% of total revenue – a powerful indicator of the recurring revenue mix. Axon’s Annual Recurring Revenue (ARR) reached $1.0 billion (+37% YoY), roughly half of total revenue. In fact, 95%+ of Axon’s business is now tied to customers on subscription plans. This subscription model provides high visibility and stability to Axon’s top line.

Recurring Revenue Quality: The growing ARR reflects Axon’s success in locking in long-term, subscription-based contracts. Dollar-based net revenue retention was 123% in Q4 – meaning existing customers increased their spend by 23% on net, with “de minimis attrition” (churn essentially near zero). Axon’s integrated bundles (e.g. Officer Safety Plan subscriptions) encourage agencies to add more devices and software over time, driving upsells. This bodes well for sustained high growth, as the company can layer new AI and cloud services onto an expanding user base of over 1 million software users.

Margins – GAAP vs. Adjusted: Axon’s gross margins paint an interesting picture. On a GAAP basis, 2024 gross margin was around 60% (slightly down from ~61% in 2023) due to heavy stock-based compensation and some one-time costs. However, adjusted gross margin (excluding stock comp and amortization) expanded to 63% in 2024, up from the low-60s prior year. The product mix and cost efficiencies are driving underlying margin improvement:

Axon Cloud & Services carries the highest margins – about 73.7% GAAP gross margin in Q4 (and 77.2% on an adjusted basis). Software is lucrative, and Axon noted its software-only gross margin exceeds 80%. The slight dip in Cloud GAAP margin (-100 bps YoY in Q4) was due to mix, but adjusted cloud margin actually rose (+150 bps YoY) on more software versus lower-margin professional services.

TASER segment margins are robust and improving. Q4 TASER gross margin was 61.3% GAAP, up 420 bps YoY. Adjusted TASER margin hit 63.7%, up 610 bps YoY, thanks to manufacturing automation, cost reductions, and the absence of last year’s one-time warranty charges. In short, the new TASER 10 is not only selling well – it’s also benefiting from economies of scale.

Sensors & Other (cameras) is the margin laggard, as hardware costs are higher. Q4 Sensors gross margin dropped to 32.8% GAAP (36.2% adjusted), a steep decline from ~47% a year ago. Why? The product mix shifted to the new Axon Body 4 camera (initial production is more costly), and Axon took inventory reserve charges on legacy products. Essentially, older camera models were written down as agencies upgrade to the latest gear. Excluding those effects, underlying sensor margins should improve as Body 4 scales, but it’s an area to watch.

Overall, Axon’s adjusted gross margin of ~63% illustrates a healthy mix of hardware and software business. As the cloud/software share grows, and as hardware production gets more efficient, the company has a clear path to margin expansion. The product mix shift toward software is a tailwind, while near-term hardware margin headwinds (new product ramp costs) are likely temporary.

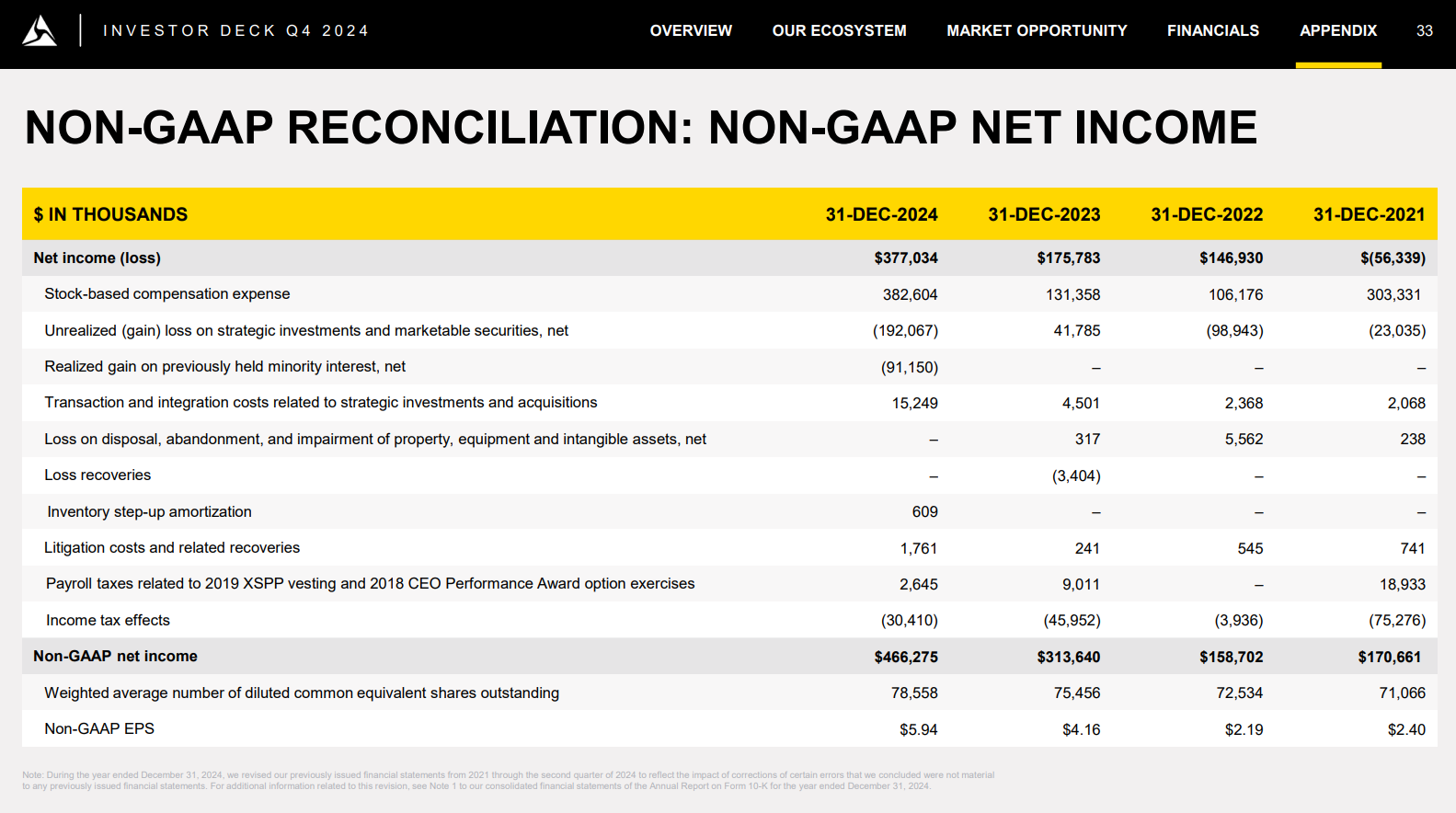

Earnings Quality – SBC and Dilution: One big caveat in Axon’s GAAP results is stock-based compensation (SBC). Axon is generous with equity grants – from broad-based employee plans to a multi-year CEO performance award – which boosts operating expenses but is excluded from non-GAAP earnings. In 2024, Axon incurred an especially large SBC expense (partly due to achieving stock price milestones): about $325 million related to the 2024 eXponential Stock Plan and CEO Performance Award. Total SBC for the year was likely much higher (Axon guides $580–630M SBC for 2025).

This impacts earnings quality. GAAP net income was $377M for 2024, a solid 18.1% net margin. But Axon’s non-GAAP net income was $466M, adding back some costs like SBC. The gap shows how much stock comp flatters the adjusted profits. It also means dilution: Axon’s diluted share count rose ~4% YoY, from ~75.5M to ~78.6M shares, as employees and executives vest shares. For investors, this dilution tempers EPS growth (though Axon’s earnings are growing so fast it outpaced the dilution). The company’s adjusted EPS was $5.94 in 2024, up 43% YoY, but on a GAAP basis EPS was ~$4.80.

Free Cash Flow & Working Capital: Axon’s earnings are translating into strong cash flows. Free cash flow for 2024 was $329 million GAAP, or $344 million on an adjusted basis (excluding minor one-offs). That’s more than double 2023’s FCF (~$148M). In Q4 alone, Axon generated $225M in free cash, an impressive cash conversion of earnings. Management highlighted a “60%+ free cash flow conversion” (FCF as a % of net income), reflecting that a large chunk of its accounting earnings are backed by actual cash.

What’s driving this cash generation? Partly the working capital dynamics of the subscription model. Axon often bills hardware up front and collects recurring software fees periodically, which can front-load cash receipts. The huge Q4 cash flow suggests strong year-end collections (agencies tend to spend budget and pay invoices by year-end). Axon’s balance sheet also shows inventory was managed roughly flat year-over-year even as sales grew, indicating efficiency gains in production and supply chain. Overall, free cash flow margin was ~16% of revenue, and Axon expects to maintain 60%+ FCF conversion going forward. This cash fuels investment and gives Axon strategic flexibility (more on that in M&A potential).

2. Segment & Business Strategy Expansion

Axon’s business spans three segments – TASER Weapons, Axon Cloud (software), and Sensors & Devices – which together form an ecosystem. Let’s break down the latest segment trends and strategy highlights:

TASER Business: Upgrading to the 10

Axon’s original flagship product line, the TASER conducted energy weapon, is experiencing a major upgrade cycle. TASER segment revenue jumped 37% YoY in Q4, as agencies rapidly adopt the new TASER 10 device. Launched in 2023, the TASER 10 offers significant improvements – double-digit cartridge capacity (up to 10 shots vs. 2 in older models like the X2/TASER 7), extended range, and enhanced accuracy. This leap in capability is driving many police departments to replace or supplement their existing stun guns. Axon shipped over 200,000 TASER devices in 2024, a record volume. While Axon doesn’t break out the mix, a large portion of those were likely TASER 10 units, indicating strong market reception.

Legacy vs. New Models: Older models (TASER 7, X2) are still being sold and supported, but TASER 10 is quickly becoming the standard. Its higher price point (and the need for more cartridges per officer) lifts Axon’s TASER revenue per user. Indeed, Axon also shipped over 9 million TASER cartridges in the year – a recurring revenue stream, since cartridges are consumed in training and field use. Pricing trends are favorable: agencies often opt for TASERs via bundled plans (e.g. a 5-year contract that includes devices, cartridges, training, and upgrades). This smooths out the cost for customers but effectively locks in future revenue for Axon. Management noted TASER growth was not just from device sales, but also “associated cartridges and services, including VR training”. Axon’s strategy is to sell TASER as a service – combining the hardware with training content (like virtual reality use-of-force training scenarios) and replacement cartridges, often on subscription. This increases the recurring portion of TASER revenue and deepens customer lock-in.

Bottom line: The TASER business is thriving. A new upgrade cycle is underway with TASER 10, leading to higher unit sales and ancillary revenue. This bodes well for 2025 as more agencies budget for the new devices. Axon’s challenge will be keeping up with demand – the company is investing in additional TASER 10 production capacity in 2025 – and continuing to innovate on its flagship non-lethal weapon (weapons R&D remains a focus for Axon’s long-term vision of reducing gun violence). For now, TASER is a growth engine and a profit center (60%+ gross margins), providing the cash to fund Axon’s software ambitions.

Axon Cloud: SaaS at Scale in Public Safety

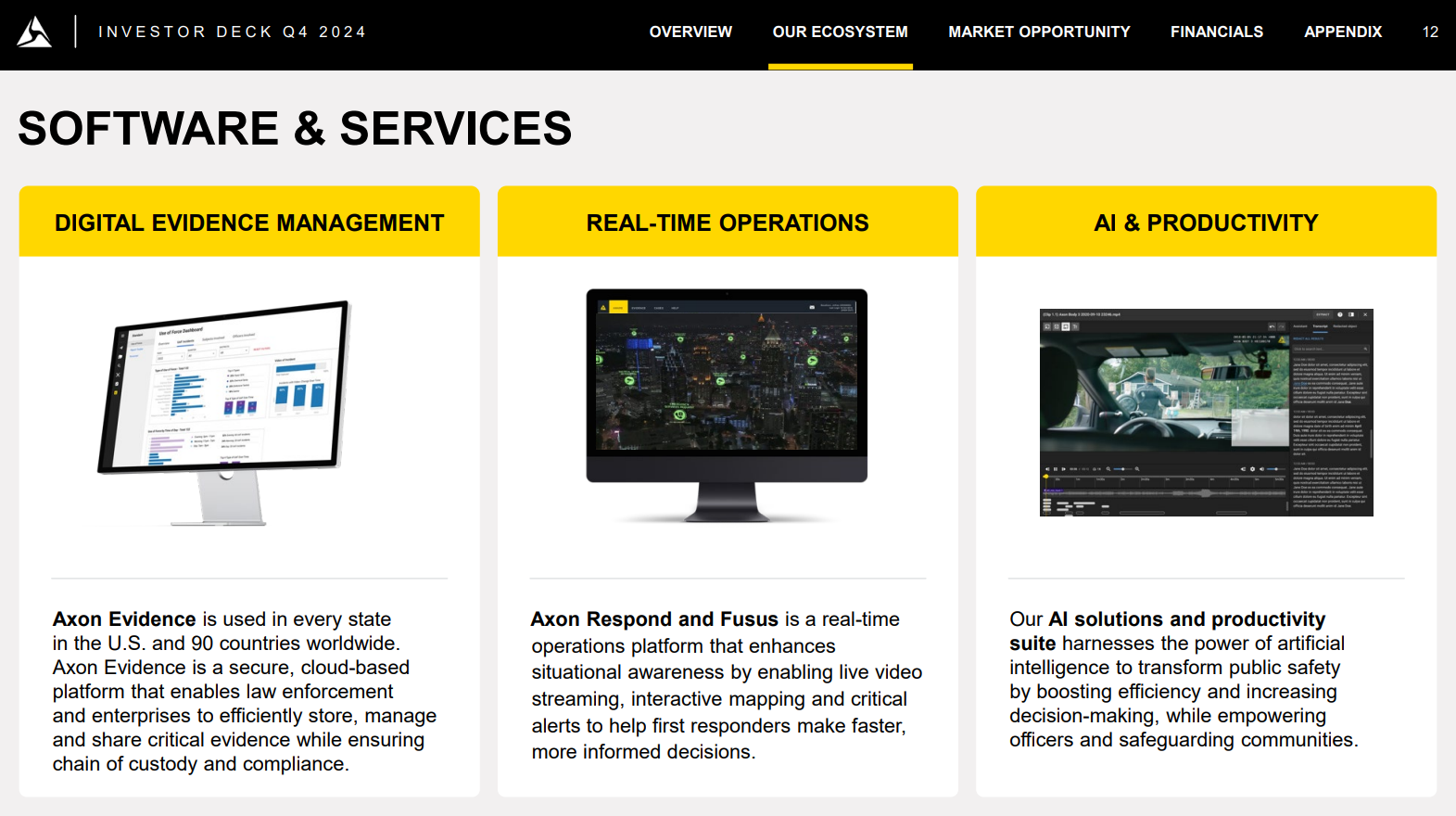

The Axon Cloud segment – comprising cloud software and digital services – is emerging as the star of the show. Cloud & Services revenue grew 44% in 2024 to $806M, outpacing overall growth. This includes a suite of SaaS offerings that police agencies (and now enterprises) use every day:

Axon Evidence: A digital evidence management system (DEMS) that stores and organizes the footage from body cameras, dash cameras, CCTV, and more. Axon Evidence has become foundational for many agencies – effectively the “cloud locker” where all video evidence is uploaded and reviewed. As Axon sells more cameras, it drives corresponding Evidence.com subscriptions.

Axon Records: A cloud-based records management system (RMS) aiming to replace legacy police incident report systems. Launched a couple years ago, Axon Records is gaining traction as departments look to modernize how they write reports and handle case files. Axon noted that integrated bundles (like its Officer Safety Plan) are spurring adoption of Axon Records and other premium software. Each new module an agency turns on means more recurring subscription fees and higher net retention for Axon.

Axon Respond: A real-time operations platform (live GPS mapping of units, status updates, alerts) that helps agencies coordinate responses. Respond ties into Axon devices like Body 4 cameras (which can live-stream) and TASERs (alerts when a weapon is deployed). It’s part of Axon’s push into real-time situational awareness.

Other cloud services: Axon Performance (analytics on officer device usage), Axon Dispatch (in early stages, for 911 call management), Auto-Transcription, and more. The company is continually adding features – often powered by AI – into its cloud suite.

Growth Metrics: Axon’s cloud business benefits from a land-and-expand dynamic. In Q4, net revenue retention was 123%, reflecting that existing software customers are expanding usage (adding new modules or more users). The churn is minimal (public safety customers rarely abandon Axon once integrated – the data network effects are strong). Axon even stated it has “de minimis attrition” in its SaaS business. Additionally, Axon’s total software user count surpassed 1 million in 2024, a milestone that includes police officers and other personnel using Axon’s cloud platform. This user base can be monetized with new applications.

A standout example is **Axon’s AI-powered **report writing tool called Draft One. Introduced in 2023, Draft One uses generative AI to help officers draft incident reports faster (by summarizing body cam footage and transcripts). It has quickly become Axon’s fastest-growing software product, contributing to over 100,000 incident reports and saving 2.2 million minutes of officers’ time in 2024. This kind of value-add drives upsell: agencies are willing to pay for time-saving AI tools. Axon has bundled Draft One and other AI features into an “AI Era” premium plan (available as an add-on to its bundles). The company indicated major AI advancements are coming in 2025 and beyond, hinting that AI will be a key part of the cloud revenue story. Importantly, Axon’s cloud gross margin (~75%+) provides lots of drop-through profit as it scales.

Retention and Churn: The stickiness of Axon Cloud cannot be overstated. Police agencies typically sign multi-year subscriptions (5-10 year deals are common) for Axon’s cloud, often paid annually. Axon revealed a $10.1B backlog of future contracted revenue, much of which is cloud subscriptions that will be recognized over time. The churn (cancellations) are extremely low – losing a major customer is rare, given Axon’s dominant position and the mission-critical nature of the software. In fact, Axon’s 123% net retention implies customers expanded usage by 23% and basically no revenue loss from churn. This is on par with top-tier enterprise SaaS companies in other industries.

Going forward, Axon Cloud’s growth will be driven by: new customer additions (international and new verticals like federal and enterprise), selling more modules to existing customers (Records, Dispatch, analytics, etc.), and potential price increases or tier upgrades (Axon has indicated it can upsell customers to higher-tier bundles which include the latest AI features).

Sensors & Fleet: Cameras, Drones, and Momentum

The Sensors & Other segment includes Axon’s body-worn cameras, in-car camera systems, and other sensor devices (like drones and virtual reality headsets). 2024 saw important product cycles here:

Axon Body 4: Axon’s latest generation body camera launched mid-2023, featuring real-time connectivity (cellular streaming), enhanced resolution, and improved usability. Demand has been strong – Axon shipped ~300,000 body-worn cameras in 2024 (includes older models as well). Many agencies that deployed Axon Body 3 cameras a few years ago are now upgrading to Body 4 to take advantage of live-streaming and offload features. Large municipal and state police deployments are in progress. For example, agencies like the NYPD, LAPD, and London Metropolitan Police (historically big Axon customers) are continually refreshing their camera fleets on multi-year cycles. Backlogs exist: Axon has openly said it’s managing phased rollouts for big contracts, which is one reason it carries a large backlog.

Axon Fleet 3: This is Axon’s in-car video system for patrol vehicles, which also includes an integrated Automated License Plate Recognition (ALPR) capability. Fleet 3 sales are ramping as police departments replace legacy dashcams with Axon’s solution that ties into the same Axon Evidence cloud. Notably, Axon’s Q4 sensor revenue growth (+18% YoY) was “primarily driven by strong demand for Axon Body 4 and Fleet”. However, Fleet installations can be lumpy (outfitting an entire fleet of vehicles often happens in batches), so quarterly revenue had some inconsistency earlier in the year. Management acknowledged some “inconsistencies in fleet revenue” in 2024 as a timing issue, but overall trajectory is upward.

New Sensor Categories (Axon Air & VR): Axon has aggressively expanded beyond body and car cameras. In 2024, it acquired Dedrone, a leader in counter-drone systems, and partnered with drone-maker Skydio to build out Axon Air, its drone-as-a-first-responder program. These moves allow Axon to offer autonomous drones that can live-stream to command centers (integrated with Axon’s cloud) and provide aerial surveillance with quick deployment. The combination of Axon Air + Axon Fūsus (real-time video platform) creates a powerful extension of the sensor ecosystem into the sky. While still an emerging revenue source, Axon Air positions the company in the rapidly growing domain of drones in public safety. Similarly, Axon’s Virtual Reality training platform (including wireless VR headsets and scenarios) falls in this segment. Axon delivered VR training as part of TASER subscriptions and is seeing good uptake for empathy-based training modules, etc. These “other” sensor products diversify Axon’s hardware lineup beyond cameras, potentially opening new enterprise and international opportunities (e.g., enterprise security drones).

Segment Outlook: The Sensors segment had a challenging Q4 margin-wise (GAAP gross margin ~33%) due to legacy inventory write-offs and the costs of ramping new products. But those are likely one-time drags. Axon Body 4 and Fleet 3 are expected to scale in 2025, which should improve manufacturing efficiency (and Axon can eventually sunset older models, reducing support costs). The demand environment is strong – law enforcement agencies worldwide are now embracing body cameras as standard issue, often driven by public accountability mandates. For instance, the UK and many U.S. states have initiatives requiring officers to wear cameras, which has generated a wave of orders. Axon’s only real competition in body cams at the high end is Motorola (WatchGuard) and a few smaller players, but Axon’s feature set and software integration give it a dominant market share.

Additionally, Axon’s order backlog includes major camera rollouts that have yet to be fully delivered, meaning there is a built-in pipeline for sensor revenue. Management has indicated some large contracts (including a huge federal security deal mentioned below) involve staged deployments of cameras and sensors over several years. Investors should expect the Sensors segment to continue mid-teens or higher growth, with possible quarterly variability, but an overall upward slope as Axon captures more agencies and upgrades. If Axon Air (drones) starts contributing meaningfully, that could add a new growth vector to this segment.

Enterprise Expansion: Beyond Law Enforcement

One of the most intriguing developments of 2024 was Axon’s push into enterprise markets – essentially, selling its tech to commercial and private sector customers for security and safety uses. Axon historically focused on law enforcement, but now sees huge opportunity in enterprise and private security, where “frontline workers outnumber public safety workers by over 20:1”. Here’s what happened:

Axon introduced Axon Body 4 Workforce – a body camera tailored for commercial use (lighter weight, and workflows for industries like retail security, healthcare, transportation, etc.) This opens up a new customer base: any enterprise that wants to equip its employees with body cameras for incident recording or safety (think private security firms, large retailers dealing with theft, ambulance companies, etc.).

Axon enhanced its Axon Fūsus platform (acquired in 2023) for enterprise security. Fūsus is a cloud software that integrates feeds from existing security cameras, sensors, and alarm systems into a real-time operations center. Enterprises can use it to monitor their facilities and, importantly, share live data with law enforcement during critical incidents. This bridges a gap between corporate security and police – imagine a shopping mall’s security cameras automatically feeding to police dispatch during an active shooter situation via Axon Fūsus.

These efforts paid off in a big way: Axon announced it was awarded the largest deal in company history from an enterprise customer. While the customer name wasn’t disclosed, this deal underscores how Axon’s TAM extends beyond government agencies. It could be a large private security company or a nationwide corporation outfitting thousands of personnel with Axon’s cameras and software. Axon noted that enterprise segment bookings tripled year-over-year, albeit off a small base. Enterprise clients often seek solutions for internal security that can interface with public emergency services – Axon is leveraging its credibility in law enforcement to win these deals.

Non-Law Enforcement Diversification: Beyond enterprise, Axon also targets federal agencies (e.g., DHS, DEA – Axon won a Department of Homeland Security body-cam IDIQ contract in 2024), corrections (prisons are adopting body cameras to reduce use-of-force incidents – Axon cites a 70% reduction in excessive force in some facilities), and even consumer/civilian markets (Axon sells a consumer Taser Pulse device and home security apps, though these are small today). The key takeaway is that Axon’s growth is expanding to new customer verticals. In 2024, U.S. state and local law enforcement still made up ~75% of revenue, but that concentration is gradually lessening as enterprise, federal, and international grow.

The enterprise push not only diversifies Axon’s revenue, it also reinforces the ecosystem. If a private business is using Axon Body cameras and Fūsus, local police benefit from that integration (they can access evidence from those cameras when needed), making Axon even more ubiquitous in public safety workflows. It also adds another dimension to the recurring revenue – enterprises will likely subscribe to Axon’s cloud services similarly to police agencies.

From an investor perspective, Axon’s ability to clone its law enforcement offerings for enterprise could dramatically expand the total addressable market (TAM). Management clearly sees this; they emphasized “enterprise” alongside federal and international as major growth vectors and noted these three groups represent over $100 billion of opportunity in TAM. The record enterprise deal in 2024 might be just the beginning of Axon becoming a default provider for workplace safety technology.

3. Operational & Strategic Insights

Beyond the quarterly numbers, Axon provided insight into its backlog, bookings, and strategic initiatives that shed light on its forward trajectory.

Bookings Bonanza & Backlog Visibility: Axon reported annual bookings over $5 billion in 2024, driving its future contracted bookings backlog to $10.1 billion (+42% YoY). This backlog (also referred to as “remaining performance obligations” plus other contracted future deals) essentially represents revenue under contract that hasn’t been recognized yet. It includes multi-year subscription contracts for software and hardware refreshes. Critically, Axon disclosed that it expects to recognize ~20–25% of this $10.1B backlog as revenue over the next 12 months, which implies roughly $2.0–2.5 billion of 2025 revenue is already “in the bag” from signed deals. Indeed, at the midpoint of guidance ($2.6B 2025 revenue), about 80-90% of 2025 revenue will come from existing backlog, illustrating exceptional visibility. The remaining backlog is generally expected to convert over the following ~10 years through contract renewals and hardware refresh cycles.

This backlog composition shows how Axon’s long-term contracts lock in customers. For instance, a 10-year Officer Safety Plan contract might commit a police agency to multiple generations of TASERs and cameras, all bundled with software each year – providing Axon a decade of recurring revenue. Investors can take comfort that Axon could likely grow north of 20% for several years just by executing the backlog (even before layering new sales). Of course, bookings growth remains important to replenish and expand the backlog, and 2024’s $5B+ in bookings (versus ~$2.1B revenue) indicates a robust book-to-bill ratio >2. Axon’s ability to consistently sign >$1B of contracts per quarter (Q4 saw record bookings, with Q4 officer safety bundle bookings nearly exceeding the prior three quarters combined) sets the stage for continued 25%+ growth.

International Acceleration: One of Axon’s strongest growth areas is international markets. Historically, Axon’s business was U.S.-centric (U.S. state & local law enforcement is ~75% of revenue). But 2024 saw a significant push overseas, and the numbers are striking. Axon’s international bookings grew nearly 50% sequentially in Q4 (on top of +40% sequential in Q3) – implying triple-digit % growth year-over-year in international sales by year-end. Key regions driving this expansion include Europe (EMEA) – especially the U.K. and other Commonwealth countries where Axon had early success – and Asia-Pacific and Latin America, where Axon is now gaining footholds. For example, countries like Australia, Canada, and several in Europe have begun large deployments of Axon cameras and TASERs. Axon’s management said 2024 was “transformative” for the international team and that they’re now landing in many new places beyond the initial English-speaking markets.

Why the sudden acceleration? A few factors:

Axon broadened its product portfolio for international. With the addition of Fūsus (real-time crime center software), Dedrone (counter-drone), and AI tools, Axon now has more to sell overseas beyond body cams and TASERs. Many international agencies are showing interest in these new solutions, especially as public safety concerns evolve (for instance, cities in Europe might invest in integrated camera networks and drones to counter terrorism or crime).

Under-penetrated markets: Axon’s updated analysis pegs international government TAM at an additional $32B+ opportunity. Outside the U.S., most police forces are not yet fully equipped with body cams or cloud evidence systems. In some countries, even TASER adoption is just beginning (Axon’s CEO Rick Smith noted that he sees a future where every officer worldwide carries a TASER alongside a firearm, and international markets could eventually mirror U.S. usage rates).

Localized execution: Axon invested in international sales and leadership, hiring regional experts (e.g., a new head for international) and adapting to local needs (language, data hosting, regulatory compliance). This is paying off in wins. There’s mention of some “inspiring” international deal in Q4 that leadership is excited about – possibly a major country-wide deployment.

Axon specifically highlighted EMEA and APAC as growth drivers. For instance, Axon won a significant contract in Germany for TASER devices (German federal police approved TASER use recently). The Middle East is another area where Axon has opportunities (some countries have large police forces looking to modernize equipment). In APAC, Axon has penetrated markets like Australia and is likely expanding in East Asia. The key point is that international revenue grew >50% in 2024 (management’s words) and is becoming a larger slice of the pie. In 2025, we could see international move from ~20% of revenue closer to 25-30% as growth there outpaces U.S. growth. This helps diversify Axon’s customer base and reduces reliance on any single country’s budget environment.

AI and Innovation at the Forefront: 2024 was a banner year for product innovation, particularly in integrating Artificial Intelligence (AI) and real-time capabilities into Axon’s platform. Management outlined “5 Big Innovative Leaps in 2024”, which are now future growth drivers:

Artificial Intelligence in Policing: Axon rolled out a suite of AI-powered features. The marquee example is Axon Draft One, the AI report assistant that significantly cuts down report writing time. They also have AI-based transcription, auto-tagging of video, redaction assistance (blurring faces in videos), and even an AI-powered training coach in development. These features enhance efficiency for customers and create upsell opportunities (the new “AI Era Plan” is an add-on subscription for agencies that want the latest AI tools). Axon indicated Draft One adoption has been rapid, and more AI features are on the way in 2025, positioning Axon as a leader in applying AI to public safety workflows.

Real-Time Operations (Fūsus): With the Fūsus acquisition, Axon now offers an interoperable real-time crime center solution. Fūsus takes video feeds from CCTV cameras, ALPR (license plate readers), drones, body cams, etc. and funnels them into one integrated platform that dispatchers or commanders can view in real-time. It’s like giving police a city-wide unified surveillance and response dashboard. Fūsus was already in use by 2,000+ cameras networks (often city downtowns or schools) and doing “millions of livestreams a year”. By integrating Fūsus with Axon’s platform (tying in Axon body cams and Respond software), Axon can sell an end-to-end real-time intelligence center to cities. This not only drives cloud software revenue, but also cements Axon’s devices as part of a broader mission-critical system. Real-time situational awareness is a hot area in public safety tech, and Axon is now at the cutting edge of it.

Axon Air – Drones & Autonomous Security: Axon’s drone initiative took off with the Dedrone acquisition (counter-drone tech) and a deepened partnership with Skydio (leading US drone manufacturer). The result is an Axon Drone as First Responder (DFR) program. Imagine an emergency call coming in – instead of (or in addition to) sending officers, a pre-positioned autonomous drone can launch and arrive on scene in 1-2 minutes, streaming video to responders. This can dramatically improve situational awareness and potentially de-escalate situations faster. Axon’s DFR solution integrates Skydio drones (for the physical hardware) with Fūsus (for the video feed) and Axon Respond. Dedrone’s technology adds airspace security – essentially detecting and tracking any drones in the area (useful for stopping malicious drones). Together, Axon Air and Fūsus provide an “eye in the sky” advantage. This capability is still nascent in law enforcement but could grow quickly; early deployments in 2024 have been promising. Additionally, drones and robotics have enterprise uses (security patrols, inspections), tying back to Axon’s enterprise expansion. With ample cash, Axon could even eventually acquire a drone hardware maker to fully own this vertical; for now, partnership suffices.

Enterprise Collaboration: Axon tailored its products for enterprise as discussed. It’s noteworthy as an innovation because it required product tweaks (e.g., the Body 4 Workforce camera) and software adaptations to meet enterprise needs. Axon’s cloud now allows businesses to run their own security operations centers and selectively share data with police. This is innovative in bridging public and private safety efforts, and Axon is relatively unique in offering it.

Mobile-First Policing: Axon emphasized making its software mobile-friendly. In 2024, it achieved FedRAMP authorization for Axon Records on mobile, meaning federal-grade security for officers to do report and evidence work via mobile devices in the field. The idea is an officer shouldn’t need to drive back to the station to type reports or tag evidence; they can do it on a smartphone or Axon’s mobile app. Mobile accessibility increases usage of Axon’s software (officers can use Draft One or upload evidence on the go), which in turn adds value to the subscription. By meeting officers where they are – literally in the field – Axon helps agencies get more out of the platform (and justify premium subscriptions).

All these innovations feed into Axon’s strategy of being the one-stop platform for modern policing. The integration of AI, IoT sensors (drones/cameras), communications, and data management gives Axon a strong competitive moat. It’s increasingly difficult for point-solution competitors to match the breadth and integration that Axon offers out-of-the-box.

4. Competitive Positioning & Market Dynamics

Axon operates at the intersection of law enforcement tech, cloud software, and defense/security – a space with few direct peers of similar scope. However, it does face competition in various areas and is influenced by market dynamics in public safety. Here’s how Axon stacks up and what could lie ahead:

Peers and Rivals:

Motorola Solutions (NYSE: MSI): Motorola is perhaps Axon’s most significant competitor across multiple product lines. The $40B market-cap giant is a leader in police radios and communications, and in recent years it has acquired companies in adjacent areas (e.g., WatchGuard for body cameras, Vigilant for license plate readers, and Avigilon for fixed security cameras). Motorola offers its own body-worn cameras and in-car systems and has a command-center software suite (dispatch, records, etc.) largely from acquisitions. That said, Axon has been eating Motorola’s lunch in body cameras – Axon’s market share and technology lead (e.g., Axon Body 4’s features vs Motorola’s cameras) keep it ahead. In cloud software, Motorola’s offerings are on-premise or fragmented, whereas Axon’s is unified and born-in-the-cloud. Axon’s 33% revenue growth far exceeds Motorola’s ~10% public safety segment growth, indicating Axon is gaining share. Motorola remains a formidable competitor due to its relationships (decades of selling to police) and broader portfolio (radios, 911 dispatch systems). But so far, Axon’s focus and innovation speed have allowed it to outrun Motorola in this space. Many agencies use Motorola for radios but Axon for cameras/cloud – a sign Axon has carved a unique leadership in the “smart weapons & video” niche.

Tyler Technologies (NYSE: TYL): Tyler is a leading provider of software to local governments, including records management and dispatch systems for police. They don’t do hardware. In records/CAD, Tyler’s legacy on-prem systems (like New World RMS) and other incumbents are who Axon Records and Axon Respond are competing against. Tyler’s growth (~7-10% annually) is much slower, and it’s transitioning clients to cloud offerings too. Axon has the advantage of bundling Records with hardware deals and offering an integrated evidence ecosystem, which Tyler cannot. However, Tyler’s deep customer relationships in city IT departments and longer history in software mean Axon has to prove itself feature-by-feature in RMS/CAD to displace incumbents. The competitive dynamic here is similar to a nimble cloud upstart (Axon) against legacy enterprise software (Tyler) – we’ve seen in other industries that cloud usually wins over time if the product is solid. So far, Axon Records is gaining traction in mid-sized agencies; winning very large city deployments will be a next challenge (Tyler currently serves many big metros for records systems).

Mark43 and Other Startups: Mark43 is a private company offering cloud-based records and dispatch software for law enforcement. It’s a closer analog to Axon’s approach (modern, cloud-first). Mark43 has won some notable city contracts (like Washington D.C.’s Metropolitan Police for records). For Axon, Mark43 represents competition on the software side in agencies where Axon doesn’t already have a foothold. However, Axon’s advantage is bundling – if an agency is already buying Axon body cams and Evidence.com, adding Axon Records might be easier than bringing in a separate vendor like Mark43. The market for cloud RMS/CAD is big enough that a few winners may coexist regionally. Axon’s main hurdle is proving the reliability and full features of Axon Records (since RMS replacement is a big decision for police departments). So far, Axon appears to be doing well, and its net retention suggests customers who adopt these new modules are happy.

VirTra (NASDAQ: VTSI) and Training Competitors: VirTra is a small company making police training simulators (think large video screens and scenarios for firearms training). Axon’s VR training content is a different approach (untethered headsets for immersive scenarios). While not a direct competitor, both target police training budgets. Axon’s VR training is relatively new but has the appeal of scalability (headsets can be deployed widely, not needing a dedicated simulator room). VirTra’s revenue (~$30M) is tiny; Axon likely surpassed that in VR training sales already by bundling it with TASER deals. This segment shows how Axon’s entry can disrupt smaller incumbents by offering a more integrated or accessible solution.

Firearms and Other Defense Tech: Axon’s mission to replace the bullet (with non-lethal) puts it in a unique competitive stance against the status quo of firearms. It’s not directly competing with Glock or Sig Sauer (firearm manufacturers), but it is trying to convince policing authorities to shift some budget from lethal weapons to TASER devices and related tech. In many cities, this is not zero-sum (they have both), but if Axon’s future higher-powered TASER devices approach firearm effectiveness, it could upend the traditional firearms market for policing. That’s a long-term scenario, but part of Axon’s narrative.

New Entrants: Given Axon’s success, one must watch for big tech or defense companies potentially eyeing this space. So far, none of the FAANG or large defense primes have made a serious play in body cameras or police cloud software – likely because it’s a niche domain with complex sales cycles. Axon’s specialization is a moat. However, partnerships are emerging (e.g., Axon’s partnership with Skydio in drones – Skydio itself competes with DJI and others; if Skydio or others decided to vertically integrate into software, they could compete, but instead they chose to partner with Axon’s network). The competitive landscape remains in Axon’s favor as the integrator of various tech for public safety.

M&A Potential – War Chest at the Ready: Axon ended 2024 with about $800 million in cash, cash equivalents and investments on hand. Even after accounting for $690M in convertible notes, Axon has over $100M net cash and no near-term debt maturities. Moreover, the company is producing ~$300M+ in free cash flow annually. In short, Axon has a $1B+ firepower available to deploy. Management has shown willingness to pursue strategic acquisitions (e.g., acquiring Fūsus and Dedrone in 2023, both presumably in the sub-$200M range). With its rising stock price and cash pile, Axon could consider larger deals ahead. Some speculative but logical areas for M&A:

AI and Data Analytics: Axon could buy a small AI startup to bolster capabilities like video analytics (e.g., gun detection in video, advanced predictive policing analytics, etc.). This would complement Draft One and Axon’s existing AI features. Any company that can accelerate Axon’s use of machine learning for public safety (while aligning with ethical guardrails) might be a target.

Dispatch / 911 Technology: To round out its platform, Axon might look at companies in the emergency dispatch or 911 call management arena. They have a partnership with RapidSOS for feeding 911 data to Axon Respond, but an acquisition of a CAD (computer-aided dispatch) specialist or 911 software firm could give Axon a native dispatch product and immediate customer base. This would pit Axon even more against Motorola and Tyler, but would fill a gap in the end-to-end suite.

Drone or Robotics Companies: While Axon has partnered for drones, it could at some point acquire a drone manufacturer or a robotics company to deepen Axon Air. For example, acquiring a leader in ground robotics (like small unmanned ground vehicles used by SWAT teams) or a stake in Skydio itself (if not a full acquisition) could secure Axon’s supply of cutting-edge hardware. Drones and robots are becoming integral to security – Axon will likely want a bigger piece of that as the market matures.

International market players: Axon might acquire regional distributors or companies overseas that have inroads with police. This could happen in markets that are tricky to enter (for example, a body-cam maker in Asia or Europe that has key government contracts – Axon could buy them and introduce its broader suite).

Adjacent Public Safety Tech: There are companies focusing on things like gunshot detection (e.g., ShotSpotter/SoundThinking), digital ticketing systems, etc. If Axon sees a chance to integrate another piece of public safety workflow (like automatic license plate readers – though they built their own ALPR in Fleet 3, or forensic analysis tools), they might buy rather than build, depending on speed to market.

With a $37B market cap and richly valued stock, Axon can also use equity for deals. Investors generally have cheered Axon’s acquisitions so far, as they’ve been targeted and quickly accretive to the product lineup. Any future M&A will be judged on strategic fit – expect Axon to stay focused on its mission (so don’t look for completely unrelated acquisitions). Given the cash on hand, we wouldn’t be surprised to see Axon announce another acquisition or two in 2025, possibly in AI or drone tech. Management has signaled that while they’re open to M&A, they remain disciplined. They’ve built a lot in-house (e.g., Axon Records was built organically) and only buy when it materially accelerates their roadmap (Fūsus is a prime example of buying rather than spending years to build a real-time video platform).

Regulatory & Policy Landscape: Axon’s growth is intertwined with public policy. Some key considerations:

Body Camera Mandates: Societal demand for police accountability has led many jurisdictions to require body-worn cameras. Dozens of U.S. states and major cities have passed legislation or policies mandating cameras for law enforcement officers, especially after high-profile incidents. These mandates are a tailwind for Axon – essentially forcing laggard agencies to adopt the very products Axon leads in. For instance, states like New Jersey and Illinois have phased-in requirements for all officers to wear cameras, which led agencies to seek vendors (often Axon due to its reputation). As more countries and departments adopt such policies, Axon stands to benefit. The recent example of the U.S. federal government: an Executive Order requires federal law enforcement agents to wear body cams; Axon promptly won contracts with DHS and others. As of 2024, body cams are far from fully penetrated (Axon estimates its TAM penetration in U.S. state & local law enforcement at under 15%). Policy changes could quickly turn the remaining 85% into active buyers.

Use-of-Force and Less-Lethal Policies: There’s a broader trend in policing toward de-escalation and less-lethal force, which aligns perfectly with Axon’s TASER business. Many police departments now mandate that officers carry a TASER or have policies encouraging TASER use before firearms when feasible. Some cities have even explored requiring officers to exhaust TASER options before resorting to a gun (within reason). Additionally, as tragic incidents occur, there’s public pressure to find alternatives to lethal force. This creates a favorable narrative for Axon – they often cite their mission to “obsolete the bullet.” However, there are also policy risks: any misuse of TASERs or health incidents (e.g., an in-custody death after a TASER deployment) can lead to scrutiny or calls to limit TASER use. Axon invests in training and smart device features (like logs and sensors in the TASER that record usage) to help agencies deploy the weapons responsibly. Another angle: Axon’s policy advisory board (ethics board) in 2022 infamously pushed back on an idea to put TASERs on drones. Axon will need to navigate the ethics and optics of how its products are used, ensuring they stay on the right side of public opinion and legal guidelines.

AI Regulation: As Axon rolls out AI tools, it must heed emerging regulations on law enforcement use of AI. For example, facial recognition use by police has been banned or limited in some jurisdictions due to bias concerns. Axon has thus far avoided integrating facial recognition into its body cameras (explicitly pausing such efforts after internal debate). Instead, its AI efforts (report writing, transcription) are less likely to draw regulatory ire. But as AI in policing grows, there could be laws requiring transparency, data security, or limits on how AI is used in decision-making. Axon will likely lean on its Ethics Board and work with lawmakers to set frameworks that allow beneficial AI (like automating paperwork) while avoiding more controversial uses. The fact that Axon is a leader here means it may help shape standards – a good position to be in – but also must be careful; a misstep (e.g., an AI error leading to an unjust outcome) could invite oversight or liability.

Privacy and Data Security: Axon hosts vast amounts of video and data on citizens. There are stringent requirements (CJIS, FedRAMP, etc.) for cloud providers in this space. Axon’s compliance track record is strong, but any data breach or mishandling of evidence could harm its reputation and bring regulatory penalties. Also, as laws like GDPR (in Europe) and various U.S. state privacy laws evolve, Axon must ensure features like its Evidence.com sharing tools have proper consent and auditing.

Budget & Funding Environment: The macro environment for government spending can influence Axon. In lean times, police budgets can be constrained, potentially lengthening sales cycles or delaying upgrades. However, public safety is typically a priority even in tighter budgets. Additionally, there is federal grant money available for body cameras and related tech (e.g., the U.S. DOJ has grant programs to help police buy cameras). Axon often benefits indirectly from such programs. A risk factor is if a recession or political shift leads to major cuts in law enforcement funding (or conversely, a “defund the police” movement in some cities). Thus far, what we’ve seen is even agencies under pressure to reform are investing in tech like Axon’s to increase transparency instead of cutting it. Axon’s backlog also insulates it in the short-medium term from any sudden budget hiccups, since many agencies have already contractually committed to purchases.

In summary, the policy/regulatory landscape largely provides tailwinds for Axon (mandates and the need for accountability tech), with some caution areas (AI ethics, privacy, budget health). Axon’s proactive stance – e.g., convening ethics panels, engaging with policymakers – shows it’s trying to stay ahead of issues rather than react to them.

5. Valuation

Stock Performance and Valuation: Axon’s stock more than doubled in 2024, and after this latest pop, it’s around $561/share with a market cap near $37.7 billion. That valuation means Axon trades at roughly:

~18x trailing 12-month sales (2.1B revenue) and about 14x forward 2025 sales (using the $2.6B midpoint guidance).

~95x trailing GAAP earnings (377M GAAP net) and around 60-65x forward adjusted earnings (assuming ~$600M non-GAAP net in 2025, which factors in growth and some add-backs).

An EV/EBITDA north of 80 on trailing basis, and ~50 on forward Adjusted EBITDA (using $655M midpoint 2025 Adj EBITDA guidance).

These multiples are undeniably high in absolute terms, especially for a company that, on the surface, sells hardware devices in addition to software. Axon’s valuation is reflective of a hybrid SaaS/high-growth tech profile:

Compared to pure SaaS/cloud companies growing ~40%, Axon’s ~14x forward sales is in-line or even a bit lower (many pure SaaS companies at similar growth trade 15-20x sales). Yet Axon is solidly profitable, which many SaaS peers are not – that can justify a premium.

Compared to defense contractors or hardware firms, Axon’s multiples are much higher. For instance, Motorola Solutions trades around 5-6x sales and ~25x earnings; body camera competitor Digital Ally (a tiny company) trades at a fraction of Axon’s multiple but with nowhere near Axon’s growth or market position. Even a high-tech defense firm like Teledyne or Lockheed is around 4-6x sales. Axon is clearly being valued more as a technology platform than a mere hardware vendor.

If we benchmark against “high-growth industrials” or companies that blend hardware and software (perhaps like Tesla in automotive tech or others), Axon’s premium still stands out.

One way to rationalize the valuation: Axon has a long runway in a relatively untapped market (its <$2B revenue is under 2% of its estimated $129B total addressable market). If Axon can continue compounding 25-30%, the forward multiples will “grow into themselves” rapidly. Still, the elevated stock price does price in a lot of good news. Any hiccup – whether a growth slowdown or margin pressure – could cause a significant rerating. So far, Axon has avoided hiccups and even macro events (like recession fears) haven’t slowed orders, given the mission-critical nature of its products.

From an investor sentiment perspective, most seem willing to pay up for Axon’s growth and market dominance. The stock’s inclusion in many growth indices and ETFs means it also gets buoyed by capital flows into growth/tech. As long as Axon executes, the investor sentiment should remain bullish, but expect ongoing debates about valuation. For example, one might compare Axon to high-growth cloud security companies (CrowdStrike, etc.) which trade 12-15x sales – Axon is in that ballpark but has a hardware element that usually drags multiples down. The counter is Axon’s hardware actually drives its SaaS, making the whole more valuable (like Apple’s ecosystem). In any case, valuing Axon requires seeing it as a category creator that straddles multiple sectors.

6. Earnings Call Takeaways & Management Commentary

Axon’s executive team, led by CEO Rick Smith and new CFO Brittany Bagley (though note: Bagley resigned in Dec 2024; a new CFO, Brittany Forsyth, was introduced on the Q4 call), provided color on the results and outlook during the earnings call. Here are the key takeaways and quotes from management, plus insight into Axon’s forward strategy:

Confident 2025 Outlook: Management struck an optimistic tone for 2025, issuing guidance for $2.55B–$2.65B revenue (+25% YoY) and $640M–$670M Adjusted EBITDA (~25% margin). This implies Axon expects to sustain the ~25% growth trajectory despite having a larger base. CEO Rick Smith highlighted that this would mark Axon’s 7th consecutive year of 20%+ growth if achieved, demonstrating the durability of demand. Key drivers for 2025 mentioned include:

Backlog execution: With $10B+ backlog, Axon has a substantial portion of 2025 revenue effectively pre-booked. CFO Brittany Forsyth noted they “baked in what is knowable” from backlog and pipeline into the guidance. The 20-25% of backlog slated for next 12 months revenue is a cornerstone of the forecast.

TASER 10 full-year contribution: 2025 will be the first year with TASER 10 available to customers for all four quarters (it was ramping in early 2024). Axon is scaling manufacturing to meet demand. This likely means higher TASER revenues, as more agencies upgrade and international orders come in (some countries that trialed TASER 10 in 2024 may place larger orders in 2025).

Subscription upgrades: Axon expects continued adoption of its premium bundles, including the AI add-on plan. With Draft One gaining popularity, they hinted that agencies will opt for the higher-tier Officer Safety Plan that includes these AI features. This not only adds revenue per user, but also cements multi-year deals.

International & Enterprise expansion: Management specifically called out international and enterprise as growth areas for 2025. Given the momentum in bookings (50%+ QoQ growth internationally in Q4, and enterprise bookings tripling YoY), they are entering 2025 with far more business outside traditional U.S. local police than a year prior. CEO Smith shared excitement about international opportunities, even teasing “one of the most inspiring days of my career” abroad that will bear fruit in the next 24 months. This likely refers to a significant international deal/initiative that isn’t public yet. Meanwhile, enterprise interest is rising as Axon’s brand recognition grows in private security circles.

Earnings Call Q&A – Risks and Nuances: During Q&A, analysts probed a few potential headwinds:

U.S. Federal Budget: One analyst asked if government budget uncertainties (like hiring freezes or debt ceiling issues) might affect Axon, especially federal contracts. Management responded that federal contracts are a small portion of Axon’s revenue and they didn’t see meaningful headwinds in that area. In other words, even if federal agencies slow rollouts, it wouldn’t dent the outlook much. State & local budgets have been stable or growing for public safety, and Axon noted they aren’t seeing signs of pullback.

International Geopolitical Upside (Ukraine): An interesting point – CFO Forsyth mentioned that none of their guidance assumes any revenue from Ukraine. This implies Axon might be in discussions to supply police/military equipment to Ukraine (likely TASERs or cameras for their forces amid the war). If something materializes, it’d be pure upside. The conservative stance here shows Axon guides on visible base business only.

Gross Margin & Costs: There were likely questions on gross margin given the sensor margin drop. Management explained the one-time inventory charges and expressed confidence that margins will normalize/improve as product mix shifts back and cost initiatives continue (especially in TASER). They also pointed out that the absence of 2023’s anomalies (like warranty charges) helped margins, and going forward, margins should be “at the right balance” of mid-60s gross and 25% EBITDA for investment vs. profit.

Operating Expenses & SBC: CFO noted they plan to keep adjusted EBITDA margin ~25%, implying they will reinvest any gross margin upside into growth (R&D, S&M). The large SBC expense in 2025 ($580-$630M guided) was acknowledged, but since Axon doesn’t guide net income, they wanted investors to focus on EBITDA and cash flow. Essentially, they’re saying “don’t be alarmed by high SBC – we account for it, but it doesn’t affect our cash or non-GAAP metrics.” Some analysts asked if the heavy use of stock comp could continue; Axon indicated these programs (XSPP and CEO award) are multi-year and tied to ambitious performance, which they view as aligning management with shareholder value creation.

Enterprise & International TAM changes: One analyst questioned what changed in Axon’s approach to boost international so much and to address enterprise. Management explained that they refreshed their TAM analysis in 2024, realizing the product portfolio has expanded, thus applicable TAM expanded (e.g., Fūsus and drones open new use cases). They see “plenty of product-market fit to be very successful internationally” and that 2024 was a turning point in building out the team and strategy abroad. For enterprise, they noted that more of Axon’s product portfolio (like cameras and sensors) is now applicable to enterprise needs, and they’re very excited to sell into that segment. Both answers basically said: we built new products, hired the right people, and now we’re executing better in these areas – hence the growth.

No Guidance Philosophy Change: An analyst asked if Axon changed its habit of guiding conservatively (since the beat was so large). CFO Forsyth said no change – they always guide based on backlog + pipeline with some cushion for uncertainty. Reading between the lines: Q4’s huge EPS beat was partly due to one-time tax benefits and investment gains, so the “core” beat was smaller. They likely won’t start guiding super aggressively; it will remain a bit conservative, which is fine by investors as long as the beats keep coming.

Long-Term Vision and “Moonshot”: CEO Rick Smith often talks about Axon’s moonshot goal: “to cut gun-related deaths between police and the public by 50% before 2033.” This was reiterated as a north star for the company. In practical terms, that means:

Equipping every officer with effective less-lethal tools (like TASERs) so they have an alternative to firearms in potentially deadly encounters.

Providing real-time intelligence and training to officers to improve decision-making (so situations don’t escalate to deadly force as often).

Engaging with communities (Axon has tools like My90 for community feedback) to build trust and reduce violent incidents.

Smith’s closing remarks on the call expressed growing confidence that in the future, it will be standard for officers (even internationally) to “carry a gun and a TASER” and use the TASER in most situations, reducing reliance on guns. This is a powerful vision – if achieved, it not only saves lives but would imply a massive expansion of TASER adoption globally.

Axon’s long-term roadmap aligns with this vision:

Next-gen TASER developments (they are surely working on a future TASER with greater range or incapacitation capability to further approach firearm replacement).

Fully integrated real-time response networks (imagine all city cameras, drones, 911 calls, and responders connected – Axon wants to be the platform powering that).

AI woven through all aspects of policing (from paperwork to forensic analysis to perhaps advisory systems that can suggest de-escalation tactics).

Expanding beyond policing into broader public safety (fire, EMS) and private safety (enterprise, personal security devices).

And notably, international and civilian markets: Axon has started selling a consumer TASER device and a home security app. In the long run (think 5-10 years), Axon could address personal self-defense more directly, especially as social attitudes evolve. If non-lethal weapons become very effective, civilians might choose them over firearms for self-defense, and Axon would be positioned to capture that market.

Key Risks Ahead: Management did outline some risks such as:

Supply Chain & Production: While much improved from 2021 shortages, Axon is ramping a lot of hardware (TASER and Body cams). Any hiccup in component supply or manufacturing could delay deliveries. They appear confident currently, even raising CapEx to expand capacity.

Competitive Bidding: As Axon enters new product areas (like CAD software or federal programs), they may face tougher competition in those niches. No explicit worries were voiced on the call, but it’s something to watch if win rates ever slip.

Legal/Litigation: Axon is engaged in or faces potential litigation (patent disputes, product liability claims, etc.). The company didn’t cite new concerns here; in fact, they won a big FTC antitrust case in 2023 regarding a competitor. Ongoing lawsuits (like a shareholder suit over the XSPP plan diluting shares) exist, but Axon treats these as normal course for a company its size.

Macro uncertainty: If a recession hit city budgets or if inflation spikes contract costs, Axon could face some turbulence. However, their backlog and multi-year contracts insulate them in the near term. CFO mentioned they didn’t see anything that would “really impact our guidance in any way” and they’ve baked in what they know.

Wrapping up the call, management exuded enthusiasm for Axon’s trajectory. They truly believe they are just scratching the surface of their addressable market (which they peg at $129B, and even that could expand as new products emerge).

For 2025, I look forward to:

Possible surprise wins (maybe Axon will announce that mystery international project or a new enterprise partnership).

Continued high growth with improving profitability (they’re balancing ~25% EBITDA margin with heavy reinvestment to sustain growth, a level they feel is the “right balance”).

New tech rollouts (AI features, maybe a preview of TASER next-gen, deeper drone integrations).

Sources:

Axon Enterprise Q4 2024 Shareholder Letter

Axon 2024 Investor Presentation

Axon Earnings Call Transcript (Feb 25, 2025)

Additional financial data from Axon’s reported results and industry comparisons.