Deep Dive: UWM Holdings Corp (UWMC)

How to play the U.S. mortgage cycle post rate cuts

Coming out of real estate private equity, the mortgage sector has always been one I track closely. It is inherently reflexive - credit availability drives housing demand, which then feeds back into lender profitability and equity values. Few industries showcase the boom-bust cycle more vividly.

Since the Fed began its hiking cycle, mortgage origination has been effectively dormant for nearly four years. With the September FOMC delivering the first 25bp rate cut, the question is simple: where is the highest convexity in this rebound? My conclusion is mortgage originators. And within that universe, United Wholesale Mortgage UWMC 0.00%↑ stands out.

This report is deliberately long and detailed. It dissects UWMC across company fundamentals, the broader mortgage sector, macro policy drivers, and direct competitor Rocket Companies RKT 0.00%↑.

I believe UWMC 0.00%↑ could be one of the cleanest cyclical convexity trades in U.S. financials.

1. Executive Summary

Core Thesis: Core thesis is the stock should go up - should go up a lot. UWMC’s dominant wholesale market share and lean cost structure position it to create value as the U.S. mortgage cycle turns.

However, high leverage (primarily through off-balance sheet financing) and a competitive pricing environment temper our enthusiasm

In our view, the risk/reward asymmetry skews favorably: UWMC’s core franchise value and 6%+ dividend yield offer downside support, while any improvement in mortgage volumes or pricing could generate disproportionate upside due to the company’s operating leverage.

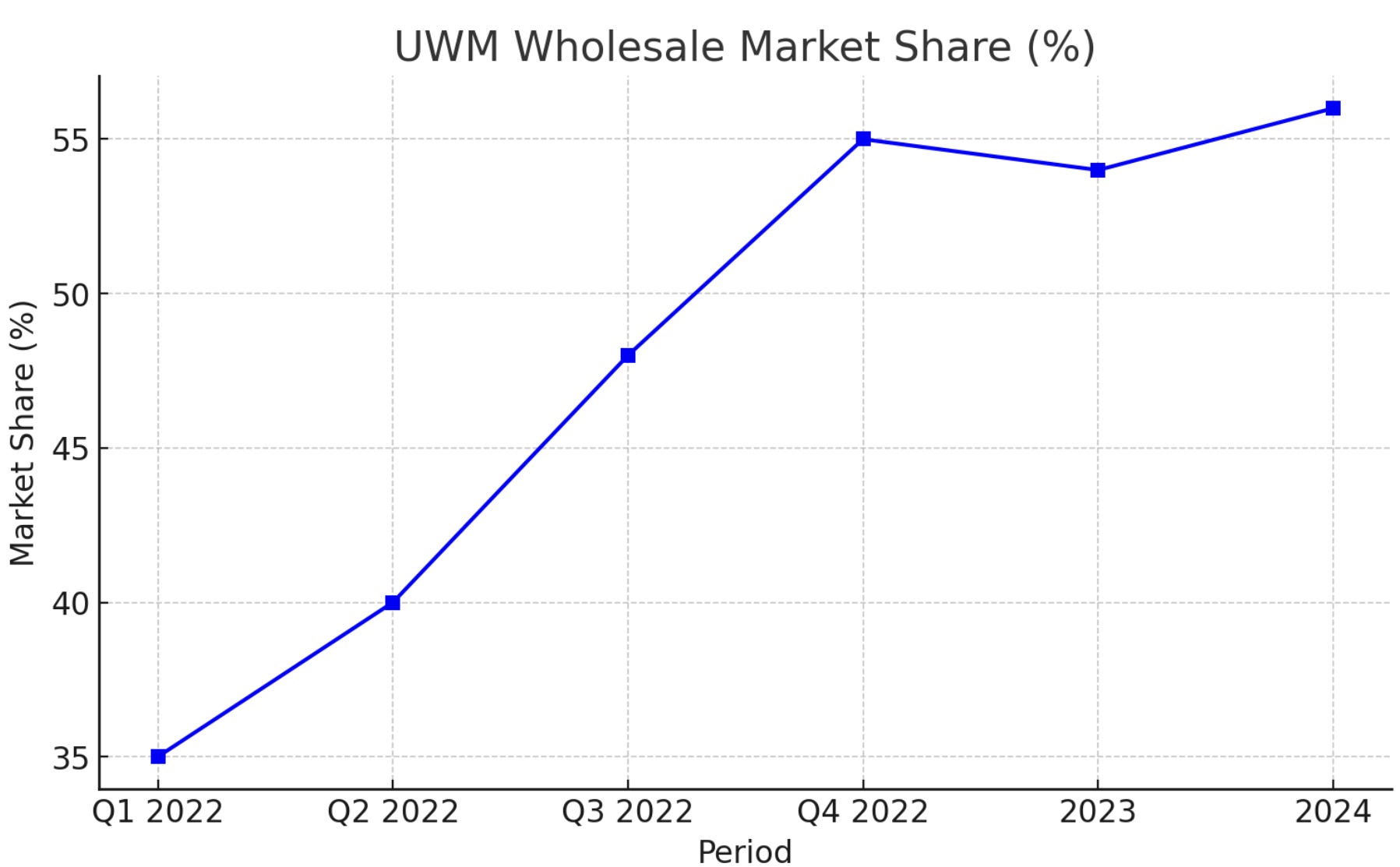

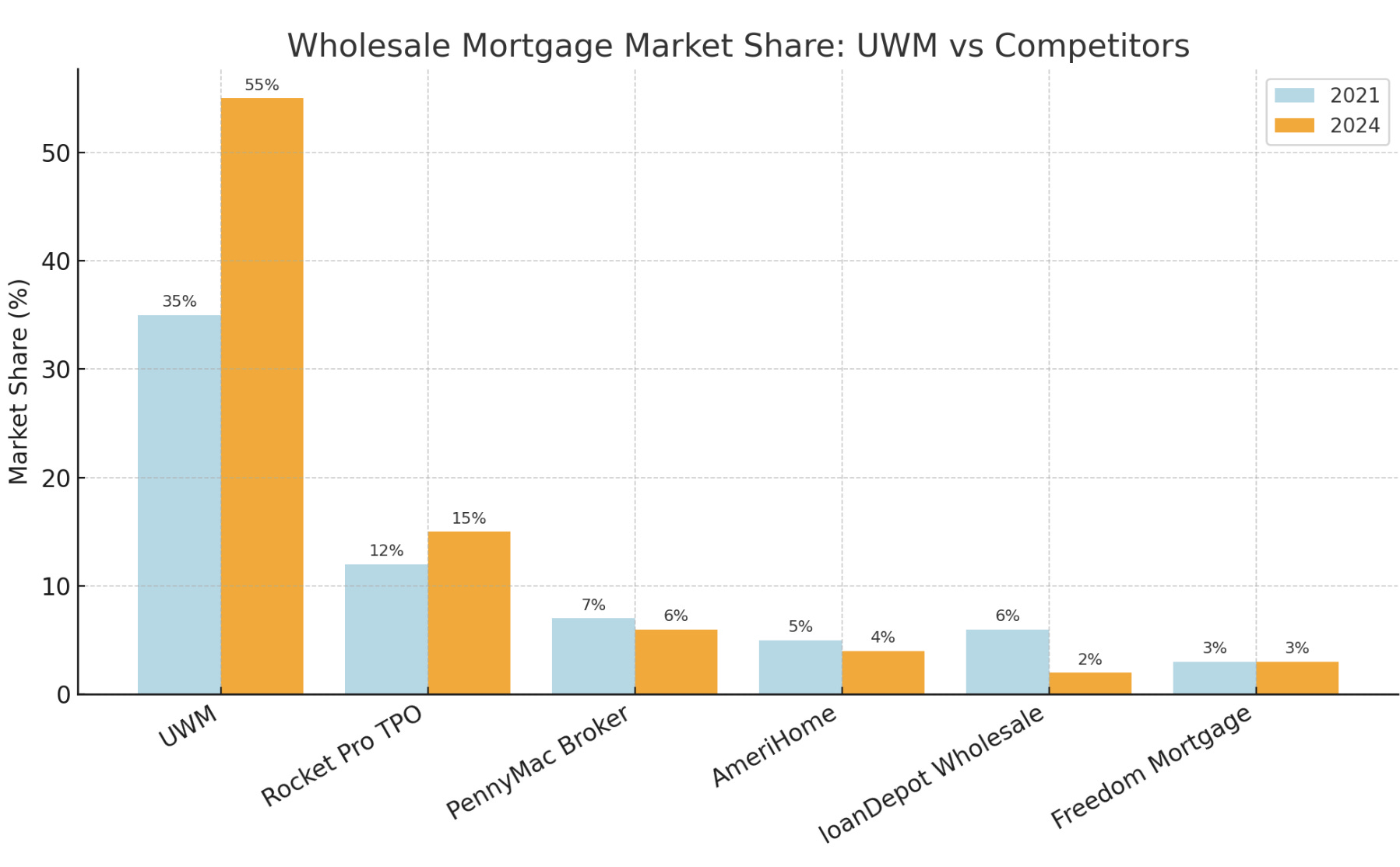

Key Value Drivers: UWMC’s value creation hinges on mortgage origination volume and gain-on-sale margins, balanced by the performance of its servicing portfolio. The company’s broker-driven model has allowed it to seize the #1 U.S. mortgage lender spot, with ~43.5% share of the wholesale channel and ~8.4% of overall U.S. mortgage originations as of 2024[1][2].

This scale advantage underpins efficiency and low unit costs. Near-term, the major drivers are:

Interest rates and refi activity - a Fed easing cycle would unlock pent-up refinance demand and boost volumes.

Housing turnover - any increase in home sales as affordability stabilizes would expand purchase originations.

Competitive dynamics - UWMC’s aggressive pricing (e.g. its 2022 “Game On” initiative slashing rates 50-100 bps) has won market share[3][4], but rational pricing returning could lift margins. Meanwhile, the company’s massive servicing portfolio (over $200 billion UPB) provides a recurring income stream and a natural hedge (MSR values typically rise when originations fall, and vice versa). Execution on technology (e.g. AI-driven underwriting tools) and maintaining broker loyalty are also critical to sustaining its moat.

Why now? Several near-term catalysts could unlock value in UWMC.

First, monetary policy inflection - the market is anticipating several Fed rate cuts in Q4 2025 - 2026, which would compress mortgage rates and potentially trigger a refinance wave (the first since 2020). Even a partial refi uptick or improvement in homebuyer sentiment would markedly increase industry volumes off today’s trough levels.

Second, competitive shakeout - many mortgage lenders retrenched or exited during the 2022-2023 downturn, leaving UWMC with fewer rivals; any evidence of pricing discipline (e.g. gain-on-sale margin stabilization) would signal better industry structure.

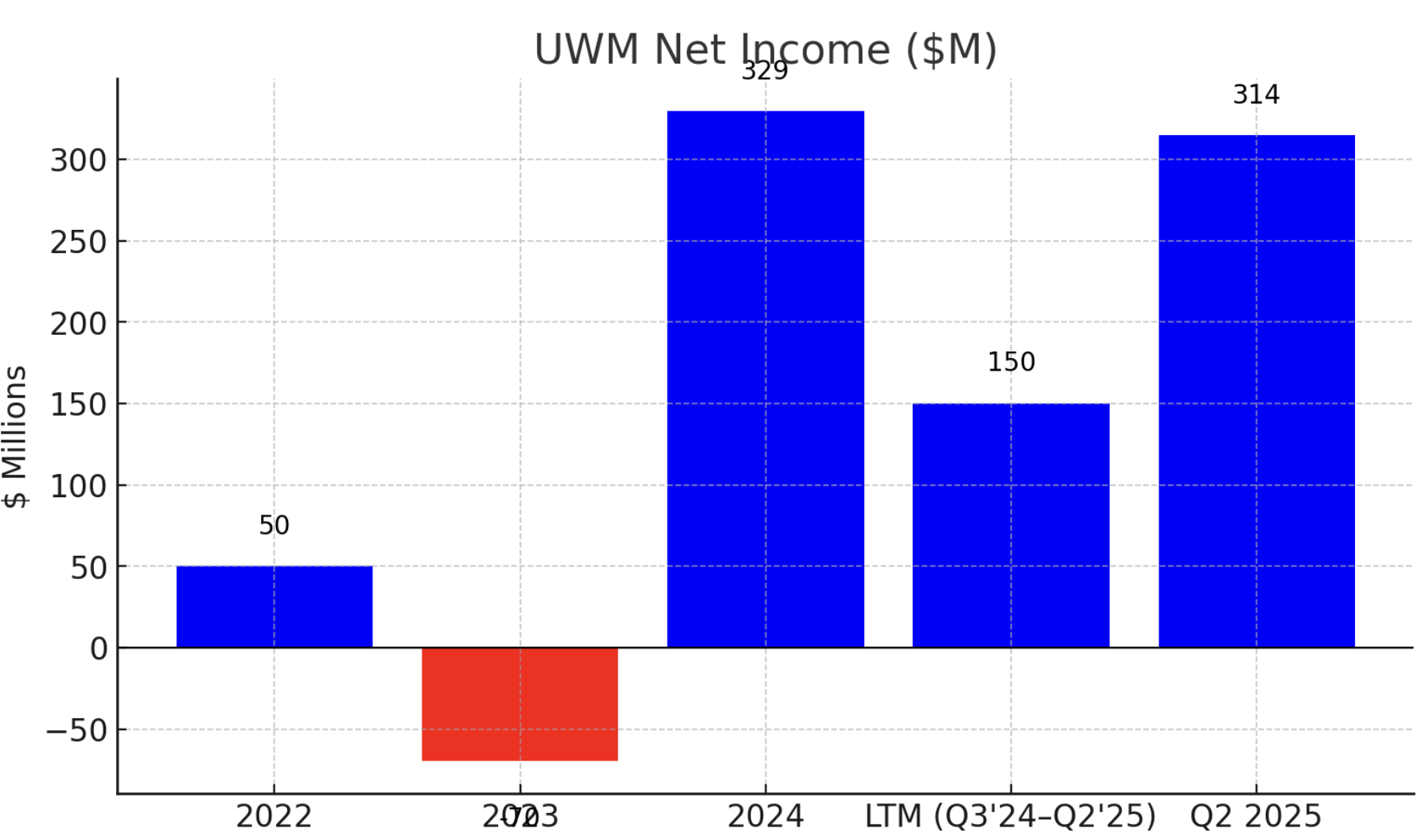

Third, earnings surprises - UWMC returned to strong profitability in 2024-2025, and recent quarters have materially beat expectations (Q2 2025 net income was $314.5M, the best quarter since 2021[5][6]). Continued outperformance or a guidance raise could prompt upward revisions from skeptics.

Lastly, capital actions - UWMC’s sustained $0.10 quarterly dividend (19 consecutive quarters as of Q3 2025[7]) and any potential share buybacks or insider purchases would underscore management’s confidence and attract yield-focused investors.

I truly do believe that the current dislocation between depressed mortgage activity and UWMC’s growing franchise presents a timely entry opportunity before broader market sentiment shifts.

2. Company Overview

UWM (United Wholesale Mortgage) was founded in 1986 by Jeff Ishbia as a family-run mortgage business (originally “Shore Mortgage”)[8]. For its first two decades, it operated as a relatively small lender.

Mat Ishbia, Jeff’s son, joined in 2003 and became CEO in 2013[9]. Under Mat’s leadership, UWM pivoted to focus exclusively on the wholesale channel - working with independent mortgage brokers rather than retail customers. This strategic focus coincided with a major industry shift: after the 2008 financial crisis, many big banks (e.g. Wells Fargo, BofA) scaled back or exited wholesale lending[10][11].

UWM capitalized, rapidly scaling its broker network and technology to fill the void. The company’s growth was explosive during the 2010s, and by 2015 UWM had become the largest wholesale mortgage lender in the U.S.[12].

It has held that #1 wholesale position for ten consecutive years now[13]. In 2020-2021, amid a record refinance boom, UWM’s volume surged and the company decided to go public via a SPAC merger.

In January 2021, UWM merged with Gores Holdings IV (a blank-check company), debuting on NYSE with an implied valuation of $16.1 billion - at the time the largest-ever SPAC deal[14][15]. Post-SPAC, Mat Ishbia retained control through a multi-class share structure.

Business Footprint: Today, UWM is exclusively wholesale - it does not originate loans directly to consumers, but rather underwrites and funds loans sourced by a nationwide network of independent brokers. The company works with over 13,000 broker shops and 55,000+ loan officers across all 50 states[16][17]. It offers a full spectrum of mortgage products, primarily agency-eligible conforming loans (sold to Fannie Mae and Freddie Mac) and government loans (FHA, VA, USDA which go into Ginnie Mae securities)[18][19]. In 2024, 89% of UWM’s originations were sold to Fannie/Freddie or placed in Ginnie Mae pools[20] - underscoring that UWM mostly operates within the standard government-backed mortgage market. The remainder includes jumbo loans and a small amount of non-QM or home equity products for specific niches[19]. UWM’s central operations are in Pontiac, Michigan (Detroit metro), where it has a single campus housing underwriting, closing, and support staff (~7,000 employees as of mid-2022[21]). This one-location, centralized model contributes to its efficiency and culture.

Management & Governance: Mat Ishbia (43) serves as Chairman, President, and CEO. He is a high-profile leader known for an intense, sports-driven culture (Mat is a former MSU basketball player under Coach Tom Izzo). His family retains majority control: Mat and trusts hold Class D shares representing ~94% of voting power. As of Feb 2025, UWM had ~1.598 billion shares outstanding split into ~158 million Class A (public) and ~1.44 billion Class D (privately held by SFS Corp, the Ishbia family entity)[22][23]. The Class D shares are economically equivalent and convertible into Class A, but carry extra votes to preserve control. This means public shareholders own only ~10% of economic interest and have minimal influence. Such governance concentration poses risks (minority investors must rely on Ishbia’s stewardship), but also aligns incentives - the Ishbia family has “skin in the game” to the tune of billions. Insiders benefit directly from dividends (Mat’s SFS Corp gets proportional distributions alongside the $0.10/share Class A dividend[24]).

The board includes Mat’s father Jeff Ishbia and a handful of allies; independent oversight is limited given the control structure. Notably, in 2021 Mat issued an ultimatum banning brokers who partner with UWM from sending loans to two competitors (Rocket and Fairway)[25]. This aggressive move sparked lawsuits and regulatory scrutiny, reflecting a governance style that some view as combative or even “win-at-all-cost.” There have also been allegations of a hard-charging work culture internally[26]. Overall, management’s incentive is clearly to maximize volume and market share (sometimes at the expense of short-term profitability, as seen in price wars).

Business Model & Revenue Streams: UWM’s core business is originating residential mortgages and selling them into the secondary market. Its revenues primarily come from:

Loan production income (gain-on-sale) - when UWM funds a loan and then sells it (either directly to Fannie/Freddie or via securitization), it earns a gain equal to the difference between the loan’s value in the market (including servicing rights) and its cost basis. This gain-on-sale is typically expressed as basis points of the loan amount. For example, in Q2 2025 UWM’s total gain-on-sale margin was 113 bps (1.13%)[6], meaning on a $300k loan it realized about $3,390 in revenue. Gain-on-sale encompasses origination fees, interest spread during holding, and the value of the mortgage servicing right (MSR) retained.

Loan servicing income - UWM usually retains the servicing rights on the loans it originates (especially on conforming and government loans). Servicing generates recurring fee income (around 25-30 bps annually on the loan balance) for handling loan payments, escrows, and customer service. As of mid-2025, UWM’s servicing portfolio was $211.2 billion in unpaid principal (about 1.4 million loans)[27][28], which provides a substantial annuity of servicing fees. However, the value of MSRs is subject to fair-value mark-to-market, which can swing GAAP earnings.

Interest income - UWM earns interest on loans held for sale on its warehouse lines before they are sold (usually a short holding period of a few weeks). Rising rates have increased the interest carry cost on loans in pipeline, but UWM largely passes that to buyers through pricing or manages via hedging.

Other - UWM has ancillary income from its proprietary technology platforms (it doesn’t charge brokers directly, but its efficient processes reduce costs), title/settlement services (e.g. it introduced in-house title alternatives like TRAC to speed up closings[29][30]), and real estate owned (REO) sales, though these are minor contributors.

Ownership Structure & Float: The public float (Class A shares) is relatively small - ~218 million shares, or ~13-14% of total diluted shares. Insiders (primarily Mat Ishbia) effectively own the rest (Class D). Institutional ownership of the float is moderate; about 58% of Class A shares are held by institutions, 11% by insiders (e.g. management owning some Class A directly), and ~30% by retail, according to recent estimates[31]. The low float has two implications:

The stock can be volatile and prone to dislocations, as evidenced by periodic retail-trading frenzies (UWMC was at times mentioned in meme-stock forums, and currently roughly 18-20% of the public float is sold short[32][33], which adds fuel for volatility or squeezes).

Traditional corporate finance moves like equity issuance are constrained - issuing more Class A would dilute the Ishbias’ stake or require converting Class D to A. So far, management has been averse to selling down their holdings, preferring to fund operations via debt and retained earnings. Overall, the tightly held ownership provides strategic stability but limits the stock’s liquidity and may lead to valuation discounts by investors who prefer stronger governance rights or float.

3. Mortgage Industry Landscape

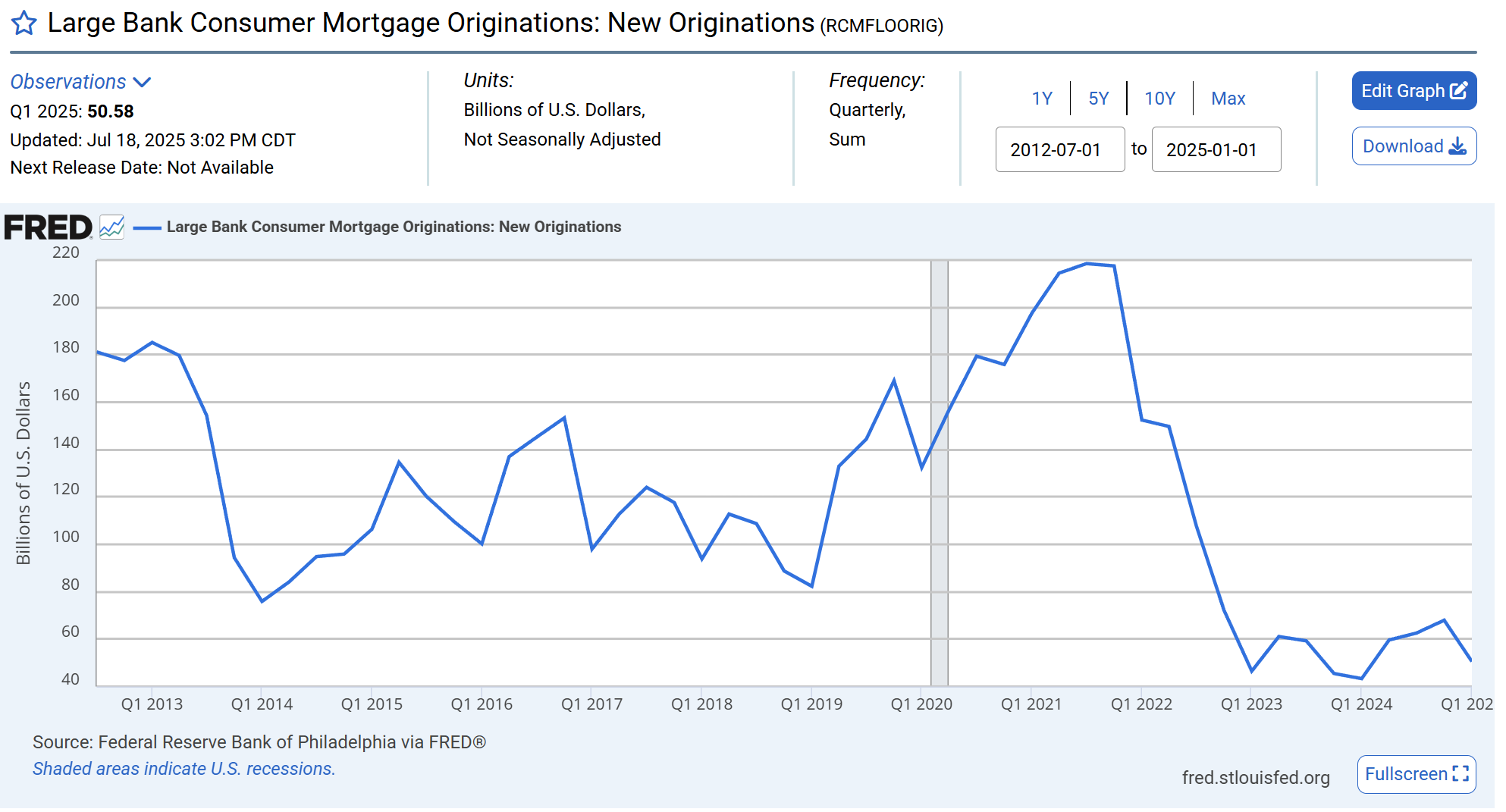

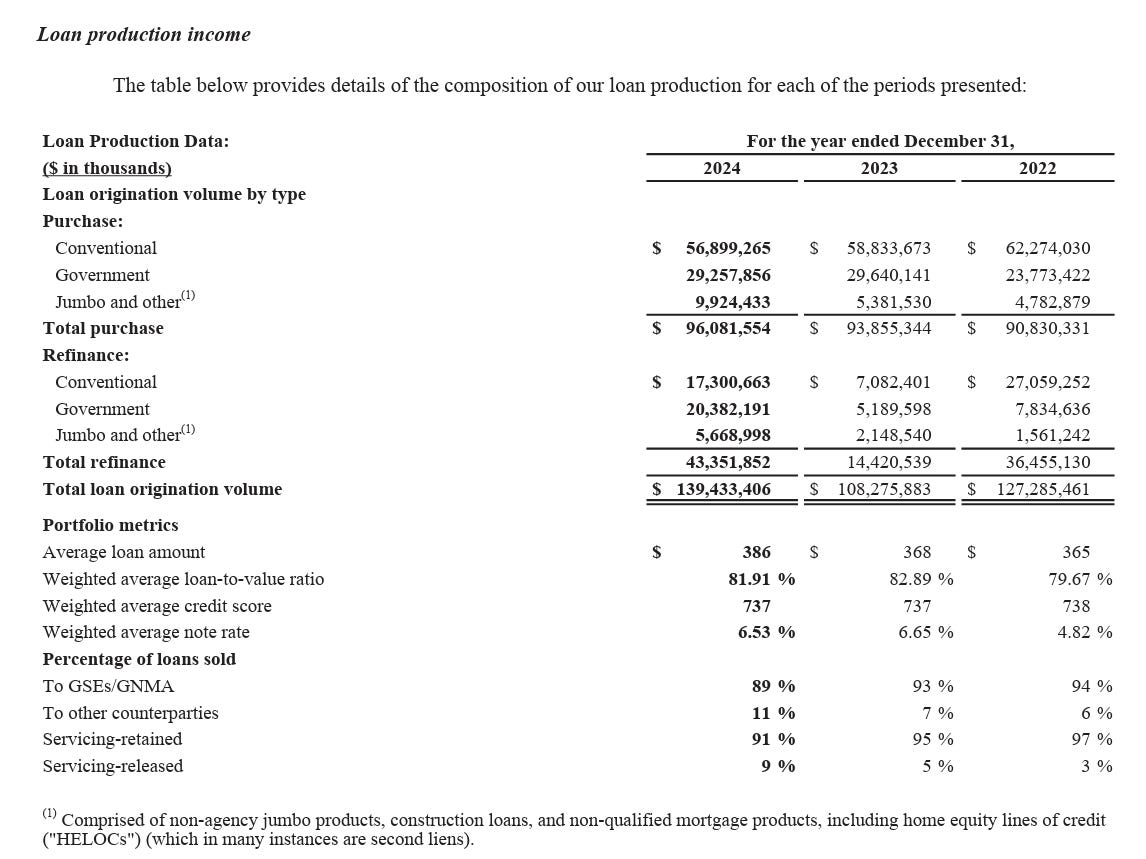

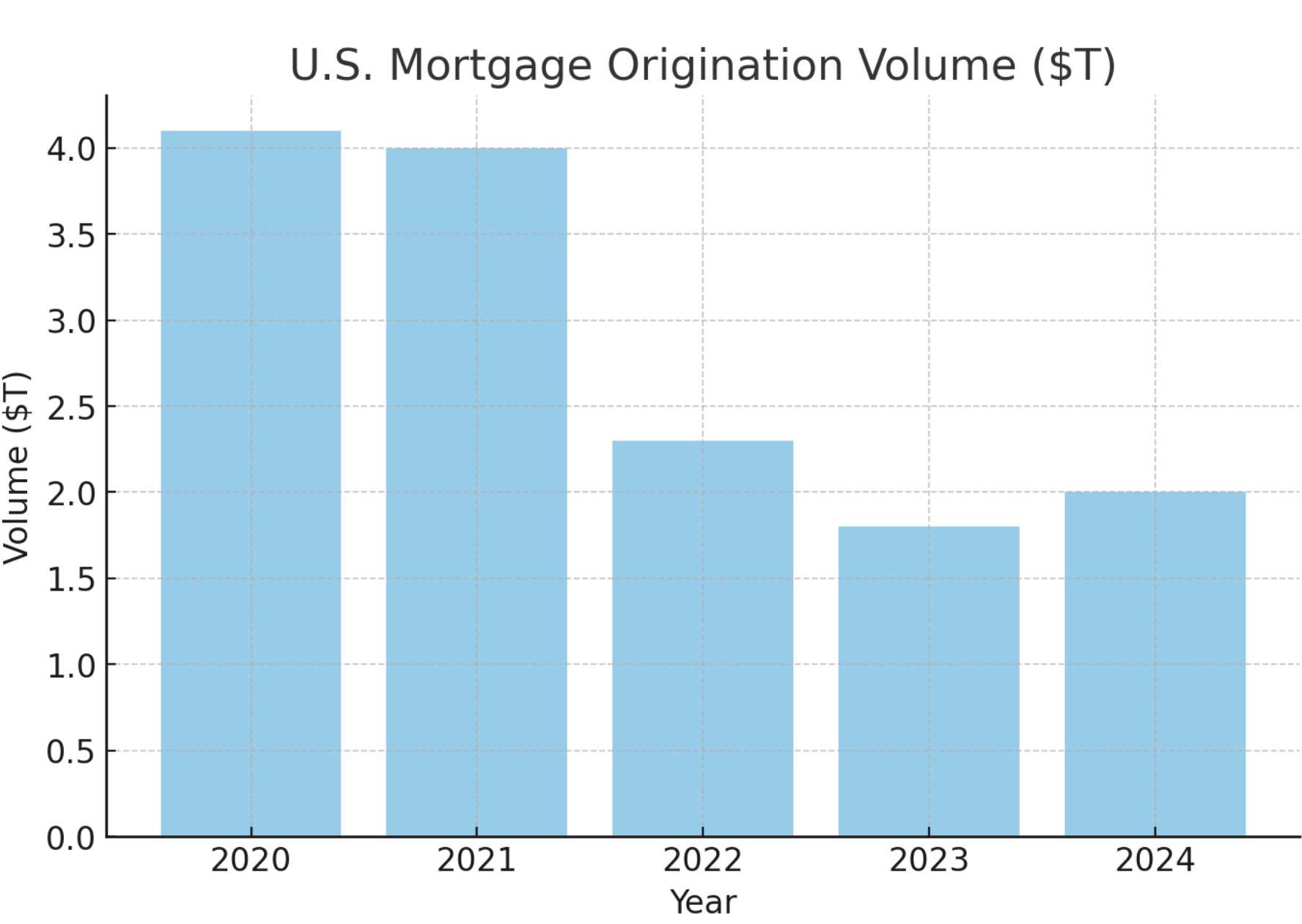

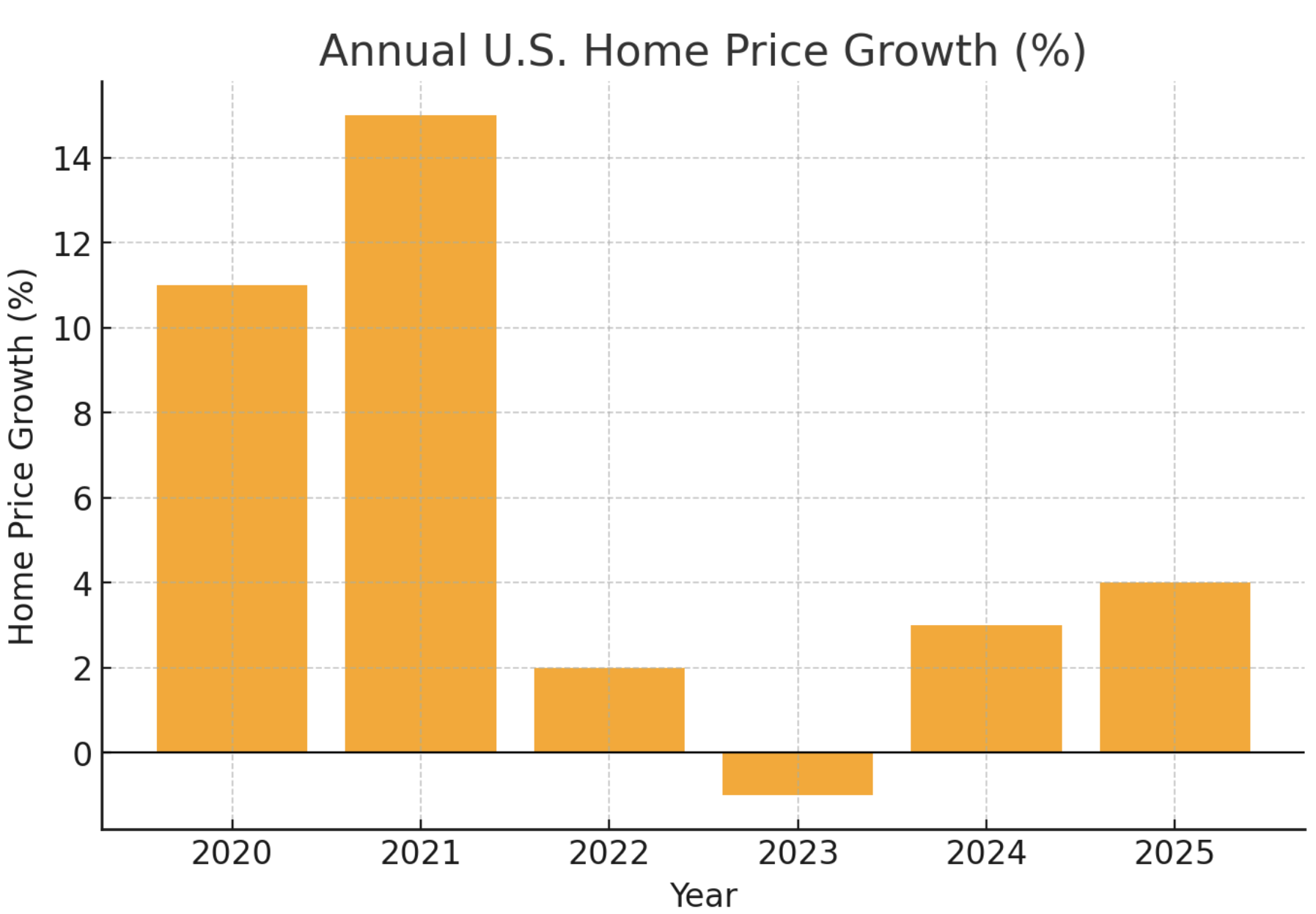

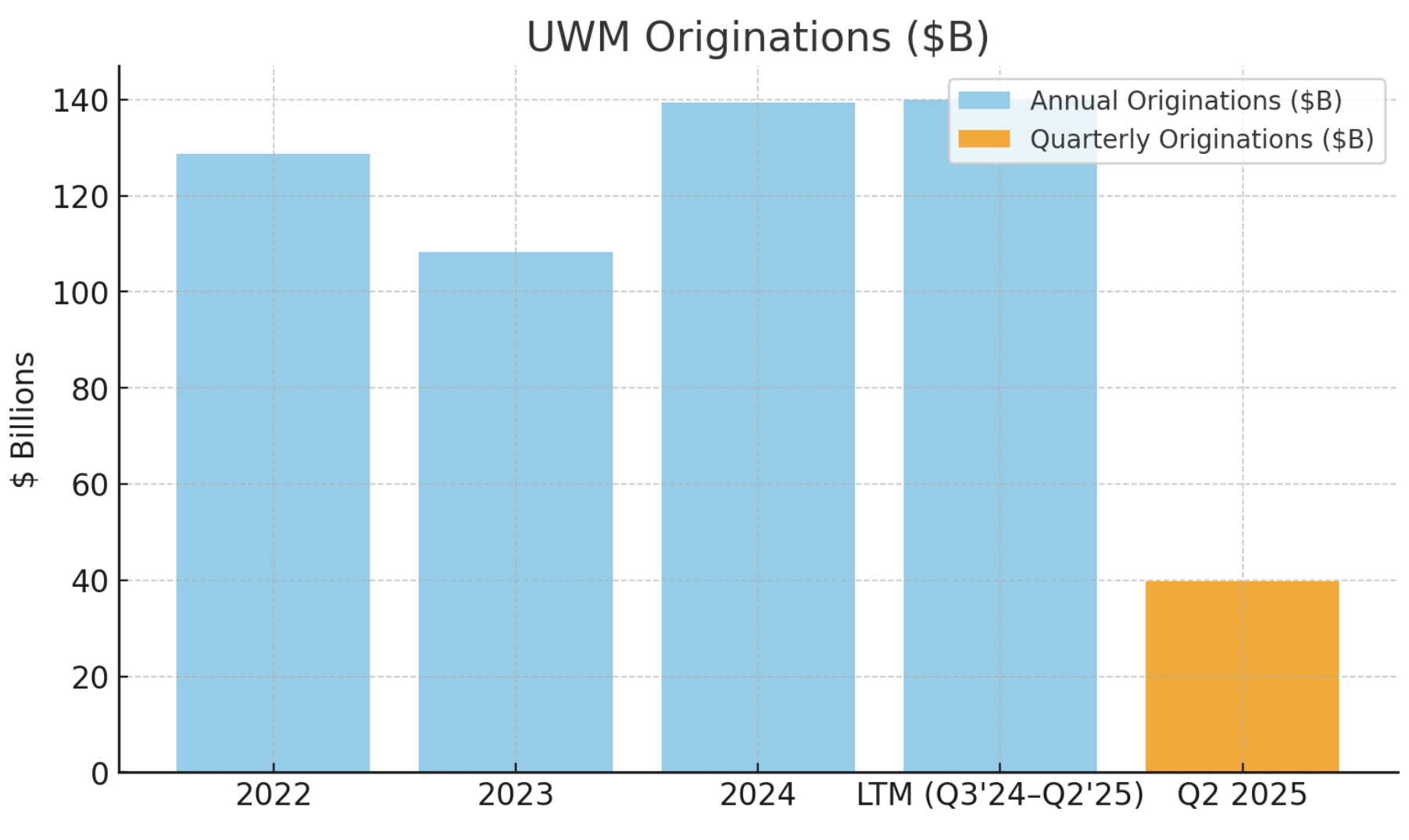

Origination Volume Cycle: The U.S. residential mortgage market is highly cyclical, swinging with interest rates and housing activity. After an unprecedented boom in 2020-2021, when 30-year mortgage rates hit all-time lows (~2.7%) and annual origination volume exceeded $4 trillion, the industry saw a sharp contraction. By 2022-2023, the Federal Reserve’s rapid rate hikes pushed mortgage rates to ~7-8%, crushing refinance demand and straining affordability for purchases. Total origination volume fell to ~$2.3T in 2022 and only ~$1.8T in 2023[34] - a steep drop (~50%) from the peak. 2023 in particular was extremely challenging: it saw the lowest existing home sales in roughly 30 years (5 million or fewer annualized) due to the “lock-in effect” (homeowners with 3% mortgages unwilling to move and give up low rates). Within this depressed market, purchase loans dominated (~75-80% of volume in 2023-24 were purchase mortgages, as refis dried up)[35][36]. Going into 2024-2025, industry forecasts (Mortgage Bankers Association, etc.) expect only a gradual recovery: purchase volume inching up with new home sales and first-time buyer programs, and refi volume remaining muted until rates drop more materially.

Retail vs Wholesale vs Correspondent: There are three main origination channels: -

Retail/Direct: Lenders (banks or non-banks) deal directly with consumers (via loan officers, call centers, or online). Rocket Mortgage is the poster child here, using a consumer-facing fintech approach.

Wholesale/Broker: Independent mortgage brokers source the borrower, then connect them to a wholesale lender (like UWM) who underwrites/funds the loan. The borrower interacts with the broker as their point of contact.

Correspondent: Smaller banks or originators make loans and then sell them to larger aggregators (like Pennymac or Wells Fargo), who then securitize or service them. Correspondent is effectively a B2B channel for closed loans.

Post-2020, market share dynamics shifted notably. The broker/wholesale channel, which had been decimated after 2008 (falling to ~10% share by 2014), made a comeback - rising to about 20% of mortgage originations by the late 2010s and holding around that level or a bit higher in recent years[37]. UWM’s leadership played a role in this resurgence: through investments in speed and pricing, UWM has proselytized the broker model (their slogan: “Broker is Better”), arguing it yields lower rates and faster closings for borrowers. Indeed, brokers have gained favor with many loan officers leaving retail banks, attracted by the flexibility of being independent. As of 2024, roughly 2 in 10 U.S. mortgages are broker-originated[38]. UWM is the clear whale in this pond - in 2024 it alone accounted for ~43.5% of all broker-originated loans[1][39]. The retail channel still commands the majority (~60-70% share including consumer-direct non-banks and depository lenders’ retail operations). Rocket historically led retail originations and overall volume from 2018-2021[40][41], but in 2023 UWM surpassed Rocket to become the #1 overall mortgage originator[42][43] - a symbolic changing of the guard. (UWM funded $108.5B in 2023 vs. Rocket’s $76.3B[44][45].) The correspondent channel is significant (particularly for banks offloading production), but UWM deliberately does not participate in correspondent. This is an important nuance: UWM only counts brokered loans it underwrites, whereas some competitors like Pennymac or Wells buy a lot of loans from smaller originators (correspondent volume) which inflates their total but with thinner margins. UWM’s stance is that correspondent lacks the relationship and service element of true wholesale.

Post-2020 Market Share Shifts: The COVID refi boom (2020-21) lifted all boats, but also sowed seeds of intense competition once volume shrank. Many new fintech lenders popped up, and non-bank lenders aggressively hired capacity. Come 2022’s downturn, a shake-out ensued: smaller and poorly capitalized lenders went bankrupt or sold (e.g., Homepoint, once a top-10 wholesale lender, shut down its originations in 2023). Depository banks like Wells Fargo, once #1 in mortgages, pulled back sharply (Wells exited correspondent entirely in 2023 and cut retail to focus on its bank customers[46][47]). This vacuum benefited survivors. For instance, UWM increased its market share during 2022-24 by staying on offense - notably launching the Game On pricing in mid-2022 which undercut competitors and grabbed volume in a shrinking pie[3][4]. By 2024, UWM originated nearly $140B (roughly 11% of all U.S. mortgages) while Rocket did ~$92B[48][49]. The next tier (CrossCountry, Chase, etc.) were far behind at ~$30-40B[48][50]. In purchase mortgages, UWM’s dominance is even more pronounced: it did $96B of purchase loans in 2024 vs Rocket’s $50B[51][52], reflecting how brokers excel in purchase markets (local referral networks) while Rocket’s refi-centric model lost ground. Conversely, Rocket had led in refinances - but in 2024 even there UWM edged them ($41.6B vs $39.8B)[53][54], a surprising flip that can be attributed to UWMC’s sheer scale and perhaps broker ability to source cash-out refis. Overall, the industry is bifurcating: a few large non-banks (UWMC, Rocket, Pennymac, loanDepot, etc.), some big bank players (Chase, Wells - albeit reduced, BofA), and many small independents. UWMC’s broker-first approach has solidified a durable niche that now is more mainstream than at any time since 2008.

Independent Broker Ecosystem: The wholesale channel’s health depends on the community of independent mortgage brokers. These are typically small businesses or individual loan officers who act as intermediaries. Post-2008, brokers faced reputational and regulatory challenges (they were blamed for pushing exotic loans; new rules like Dodd-Frank’s LO Comp rule banned yield-spread-premiums that incentivized higher rates). However, with those reforms, brokers re-emerged offering borrowers a “shopping” advantage - they can find the best rate among many lenders. UWM has nurtured this ecosystem: it provides brokers with free technology (like its EASE underwriting portal and BOLT instant title system[55][56]), marketing support (Brand 360 tools), and even leads (its consumer web Mortgage Matchup directs borrowers to brokers[57][58]). UWM’s relationship with brokers is symbiotic - brokers rely on UWM’s fast turn times (as low as ~16 business days from application to clear-to-close, vs 40+ days industry average[59][60]) and pricing, while UWM counts on brokers to bring in business. A potential risk is broker consolidation or attrition: when the market shrank, many LO’s left the industry. There were ~360k registered mortgage loan officers in the U.S. as of Sep 2024[61], but many are dormant. If broker ranks dwindle or if big lenders try to poach brokers in-house (e.g. retail lenders recruiting top broker shops to become branches), that could impact UWM. So far, the trend has favored independence, with some large teams leaving banks to start brokerage firms given UWM’s support. Additionally, regulatory changes (see below) could influence the broker model viability (e.g. any cap on broker fees or disclosure changes might hurt competitiveness).

Cyclical Drivers: Several macro factors drive mortgage volume cyclicality:

Interest Rates (Refi vs Purchase Mix): In low-rate environments, refinancing dominates (borrowers replace higher-rate loans with new ones). In high-rate environments, almost no one refinances unless they must (cash-out or divorce, etc.), so the market skews to purchase loans. UWMC’s historical strength was actually in purchase loans - even during refi waves, it kept focus on purchase (it has been #1 purchase lender for 4 years straight through 2024[62][40]). This provides some resilience; purchase volume is less rate-elastic (people still buy homes due to life events). That said, overall volume is far higher when refis are active. A drop in mortgage rates from ~7% to, say, ~5% could unleash tens of millions of refinanceable loans, dramatically expanding industry volume and benefitting all lenders including UWM. Conversely, if rates were to spike further or stay at ~7-8% for years, the purchase market alone may not fill the gap, and originators would face prolonged low volumes.

Housing Turnover & Affordability: The number of home sales (turnover of the housing stock) directly drives purchase mortgages. Currently turnover is historically low - existing homeowners are locked in with low rates, and new listings are scarce. Housing affordability indices (combining home prices, rates, and incomes) fell to multi-decade lows in 2022-23. Any improvement on this front (through either modest home price declines, income growth, or lower rates) could boost sales. Homebuilders are one bright spot - they increased new construction and often subsidize mortgages (rate buydowns), which has funneled more buyers to builders and their captive lenders[63]. UWM’s exposure to builders is indirect (some brokers work with new home buyers, but builders often steer to their own lender). So a risk is if a structural portion of purchase volume shifts to builders’ in-house lenders (e.g. D.R. Horton’s DHI Mortgage, which ranked #7 overall in 2023[64][52]). However, that is a segment UWM historically hasn’t dominated, so its growth or decline may not greatly affect UWM’s base.

Credit Availability: Mortgage underwriting standards (credit scores, down payments, debt-to-income limits) expand or tighten with the cycle. Currently, standards are relatively conservative (average FICO on UWM’s 2024 originations was likely in high 700s for conforming, >720 for FHA). If the credit box loosens (through GSE policy or competition), more borrowers qualify, boosting volume. UWM itself launched some non-QM products (e.g. Bank statement loans for self-employed, DSCR loans for investors[65][66]) to capture niches. Yet these remain small scale - UWM is not a subprime or large non-prime player. So macro credit changes (like FHA lowering premiums, or GSEs raising DTI caps) could incrementally help volume.

Home Prices: Rising home prices increase loan sizes and hence total volume (in dollar terms). In 2020-21, double-digit home price appreciation contributed to record origination dollar volumes. In 2022-23, home price growth stalled or slightly declined in some regions. UWM benefits from higher loan balances (it increases revenue per loan and makes servicing rights more valuable), but extremely high prices hurt affordability and transaction count. A gentle home price appreciation rate (say 2-4% annually) is probably ideal for a stable volume growth without choking buyers out.

Regulatory Backdrop: The mortgage industry is heavily regulated, and several ongoing or proposed policy changes could impact UWM:

FHFA and GSE Policies: The Federal Housing Finance Agency (FHFA) oversees Fannie Mae and Freddie Mac, which purchase the bulk of UWM’s loans. FHFA periodically tweaks fees and eligibility. For instance, in 2023 FHFA adjusted Loan-Level Price Adjustments (LLPAs) to favor certain borrower profiles (controversially raising fees on some higher credit tiers to cross-subsidize lower-income borrowers). Changes in GSE conforming loan limits (which rise with home prices) also affect UWM - higher limits allow it to originate larger loans under agency programs. FHFA’s push for GSE capital (part of “GSE reform” to eventually release Fannie/Freddie from conservatorship) could mean higher guarantee fees over time, raising costs for borrowers. UWM, like all lenders, would see rate sheets go up if g-fees rise, potentially dampening volume. On the flip side, any credit easing by FHFA (for example, recent talks on allowing 40-year loan terms or higher debt ratios) can enlarge the borrower pool.

CFPB and Broker Rules: The Consumer Financial Protection Bureau regulates mortgage origination practices. The CFPB’s LO Comp rule currently prevents varying broker commissions based on loan terms, which is intended to protect consumers. There is some industry lobbying to loosen these rules (e.g. allow brokers to voluntarily cut their fee to match a competitor’s offer - currently difficult due to anti-steering rules). If CFPB provided flexibility, brokers could be even more competitive on price. However, any aggressive enforcement by CFPB on broker practices (for instance, if they revisited the legality of UWM’s broker ultimatum or scrutinized broker steering) could pose operational headaches. CFPB also mandates disclosure like the Loan Estimate which brokers must provide - these compliance burdens are status quo.

Basel III Endgame (Bank Capital Rules): U.S. banking regulators (Fed, OCC, FDIC) have proposed implementing the final “Basel III” capital reforms, which include punitive treatment for mortgage servicing assets (MSRs). Under current rules, banks already face a 10% Tier 1 capital cap on MSRs (excess above which must be deducted) and 250% risk-weighting. The new proposal would effectively raise risk weights significantly (potentially 400% in some cases)[67][68]. This makes MSRs even less attractive for banks. The practical upshot: banks will likely continue shedding or avoiding MSR holdings, leaving non-banks like UWM to scoop them up. UWM could benefit because fewer bank competitors in servicing means less competition to acquire MSRs and potentially better pricing when UWM sells excess servicing. Also, banks pulling back from mortgage lending (since capital costs rise for mortgages and MSRs) could further cede market share to non-banks. However, one risk is if capital rules indirectly tighten warehouse lending (banks might allocate less to providing credit lines to mortgage lenders if overall mortgage assets have higher capital cost). We will monitor if Basel Endgame causes any strain on warehouse availability or pricing.

GSE Reform and Conservatorship End: A long-simmering issue is whether Fannie Mae and Freddie Mac will exit government conservatorship and what their role will be. Any major reform (unlikely before 2025 elections) could alter the secondary market. If, for example, privatization led to reduced guarantees or higher fees, mortgage rates could rise and non-guaranteed private label markets might revive. UWM, given its scale, could adapt by issuing more private securities or adjusting its loan mix. But generally, UWM thrives in the current system of robust GSE and Ginnie Mae support - it allows an originator-focused company to offload credit risk easily. Sudden GSE changes are a longer-term uncertainty rather than imminent.

State Regulations and Others: UWM operates in all states, subject to state lending laws. Some states have broker-specific rules (licensing, maximum fees). Additionally, UWM’s loans must comply with federal laws (TILA, RESPA, ECOA, etc.). A noteworthy regulatory hot topic is fair lending - ensuring minority and low-income borrowers have access. Non-bank lenders like UWM are under the microscope for any disparate outcomes (e.g. higher denial rates). Any enforcement action or need to alter practices (say, more costly manual underwriting to comply) could add costs. Also, agencies like the FHA and VA can change program rules (recently FHA considered 40-year loan mods, etc.) which flow through to originators.

In sum, the industry context for UWM is one of cyclical trough with structural shifts: volumes are bottoming, the broker channel is ascendant again, and regulatory currents are mostly status quo or slightly favorable for non-banks. The key external swing factor is the path of interest rates - which we detail in the Macro section - as that will dictate how quickly the mortgage tide rises from here.

4. Competitive Positioning

UWM’s competitive strategy centers on a simple premise: dominate the wholesale channel by being the fastest, most reliable, and lowest-cost lender for brokers. This strategy has yielded a sizeable moat, though not one without challenges.

Strategic Moat - Broker Relationships & Service: UWM has deeply entrenched relationships with independent mortgage brokers nationwide. Many brokers essentially consider UWM their primary partner. Why? UWM offers a compelling value proposition to brokers:

Speed and Operational Excellence: UWM’s average loan clear-to-close is ~16 business days, less than half the industry average of ~40 days[69][60]. It achieves this via a single-site “factory” approach and heavy tech automation in its proprietary LOS (the “Easiest Application System Ever” - EASE™)[55][56]. Brokers know that if they send a loan to UWM, it’s likely to close quickly and smoothly, which is critical for their reputation with realtors and borrowers.

Technology Suite: UWM continuously rolls out broker-centric tech tools. Aside from EASE, there’s BOLT (for near-instant underwriting of appraisal and title components), UClose (which lets brokers schedule exact closing times and generate closing docs in minutes), and consumer-facing Blink (a white-label application portal brokers can give clients). In 2023-25, UWM invested in AI bots (“Mia” for underwriting assistance, “LEO” for identifying conditions, etc.) to further streamline processing[70][71]. These tools are provided at no cost to brokers, subsidized by UWM’s scale. Competing wholesale lenders often cannot match this tech investment, and retail lenders don’t share their tech with third parties. Thus, brokers aligned with UWM have a tech edge in efficiency.

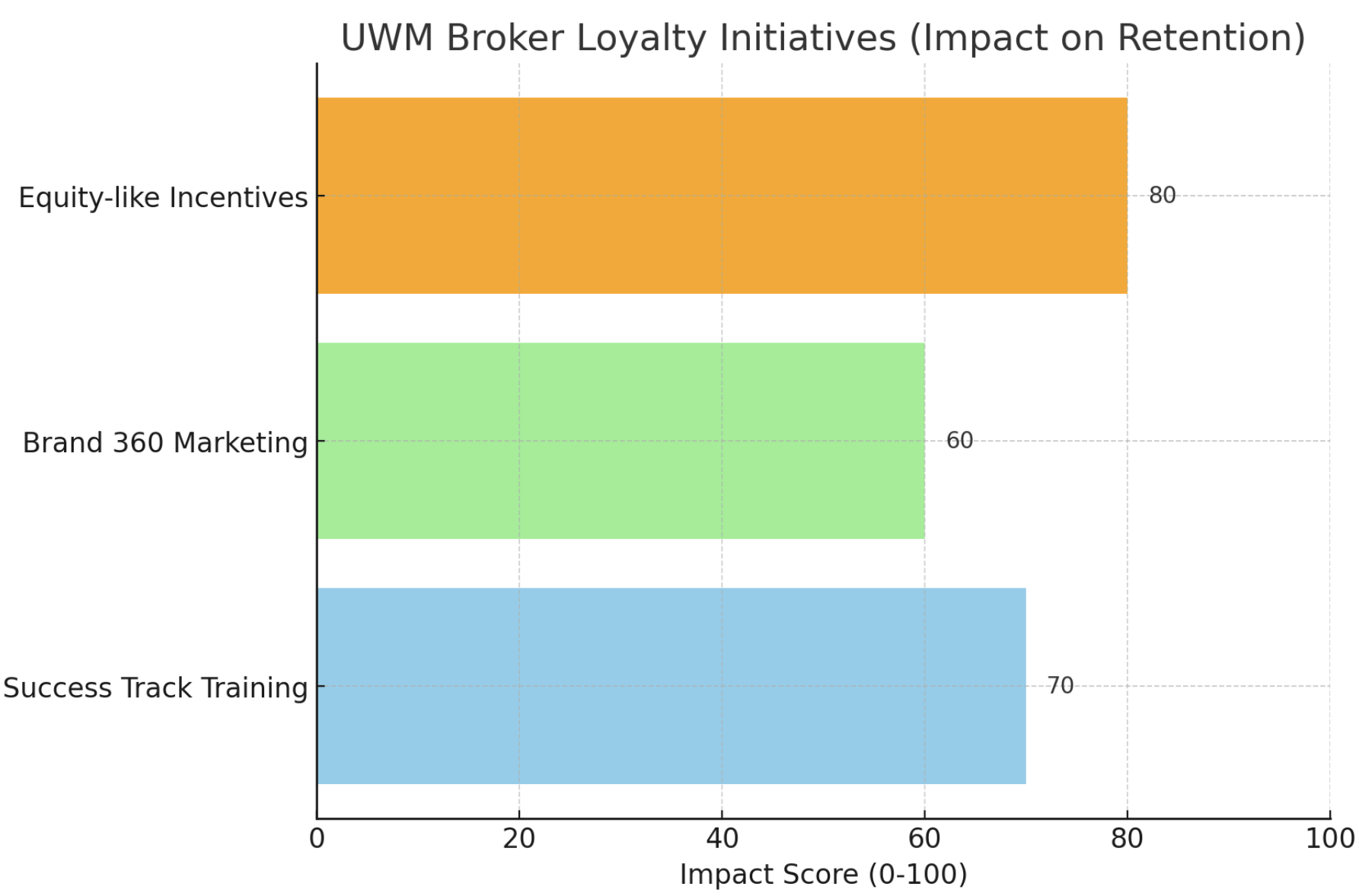

Broker Loyalty Programs: UWM has introduced initiatives like “Success Track” training for new broker shop owners, marketing support via Brand 360, and even equity-like incentives (in 2022 they floated a plan to offer brokers options in UWMC stock as a loyalty reward). All of this is aimed at cementing loyalty and switching costs - a broker who has learned UWM’s system and built a workflow around it may be less inclined to send loans elsewhere unless absolutely necessary.

Product Breadth and Niche Offerings: While UWM mostly sticks to plain-vanilla loans, it has shown agility in introducing products that brokers ask for, within reason. For example, they rolled out temporary buydown loans (where the seller can pay to lower the rate in the first 1-2 years - useful in high-rate environments), home equity lines, and the 1% down payment program (UWM grants 2% to supplement a borrower’s 1%). These programs help brokers have answers for borrowers that might otherwise go to competitors with special deals. Rocket, in contrast, often markets its own exclusive programs to consumers; UWM essentially arms brokers with similar ammunition.

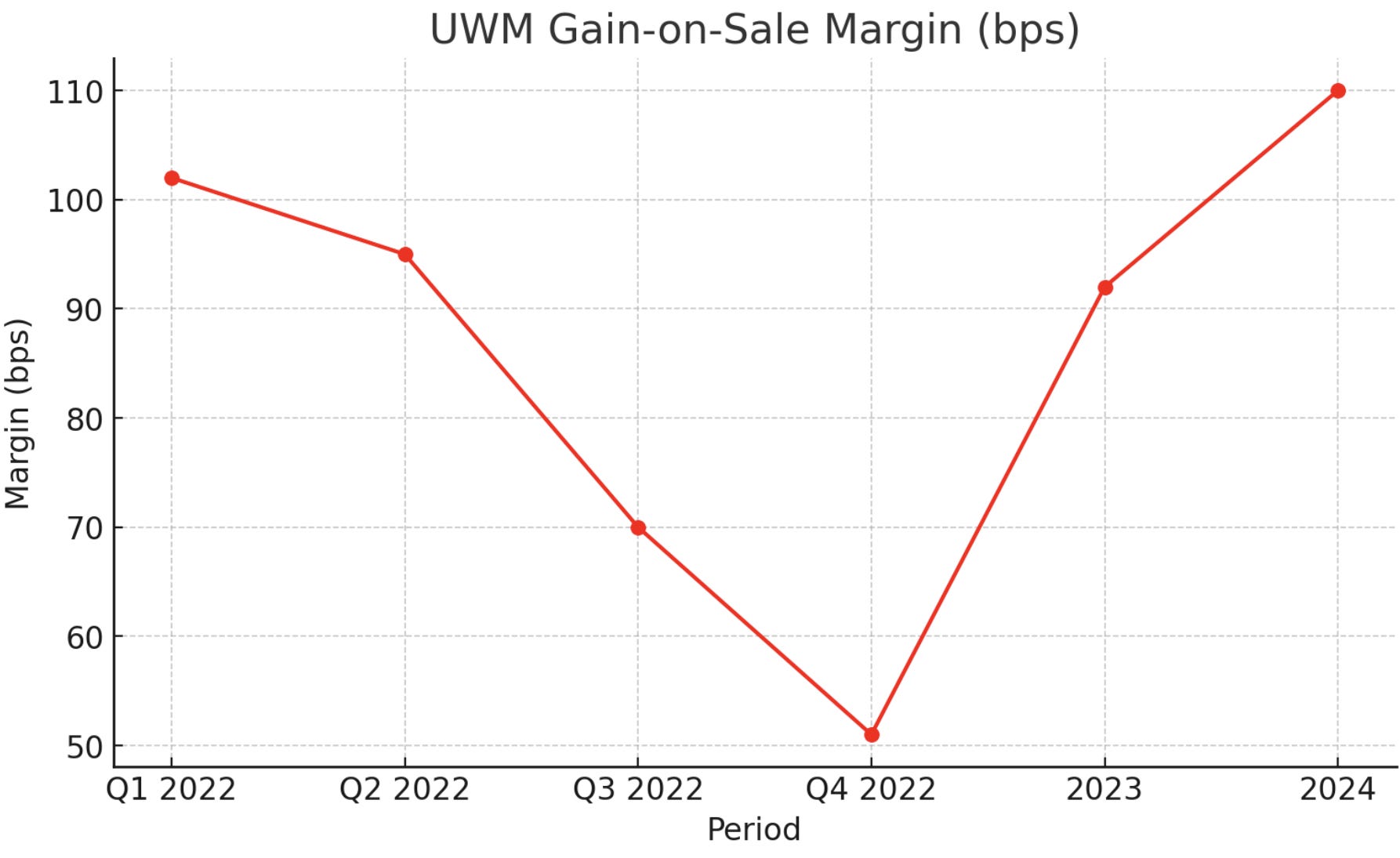

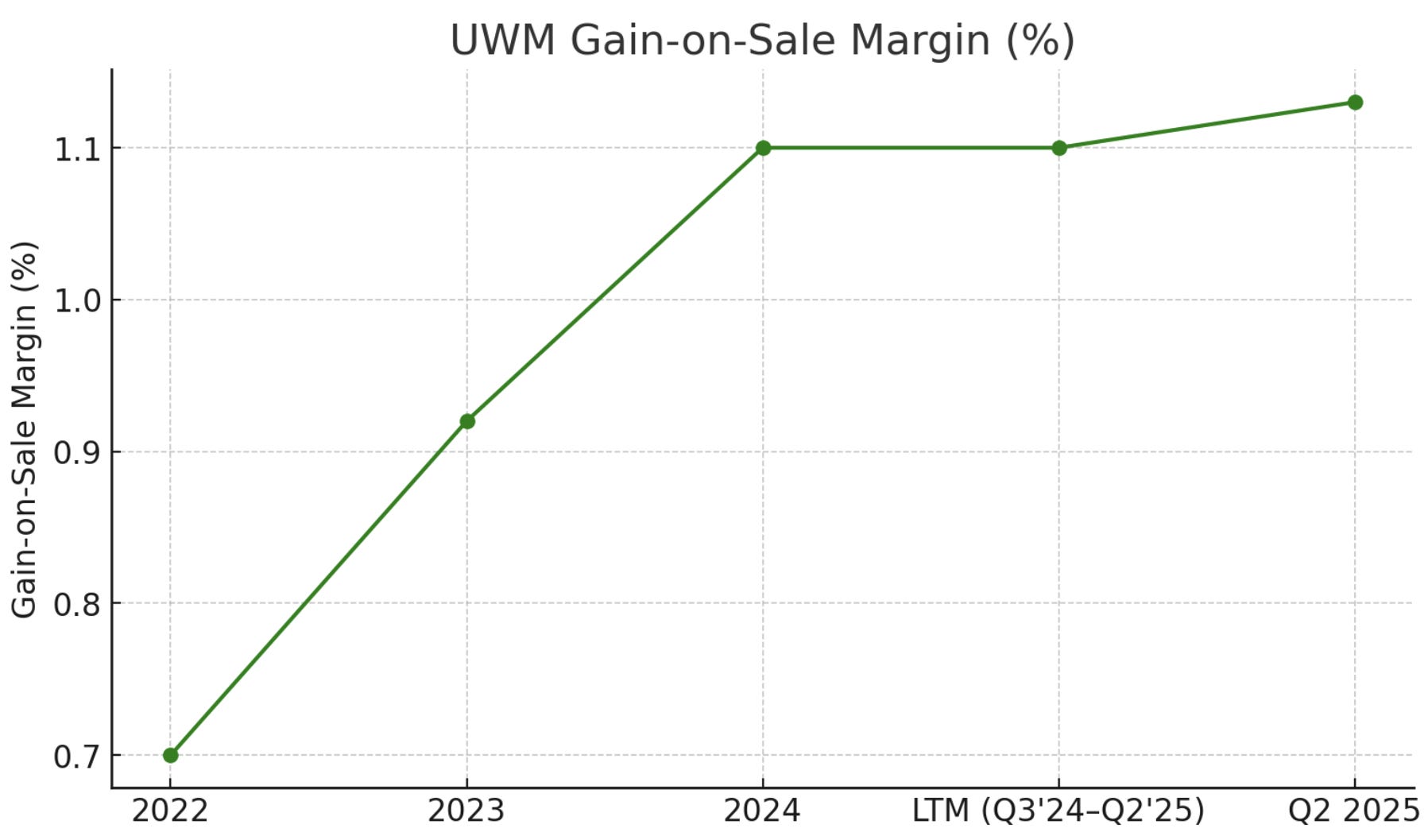

Pricing Aggressiveness: Perhaps the most talked-about aspect of UWM’s strategy is its willingness to compete on price (i.e., lower rates to the borrower, which translates to thinner gain-on-sale margins for UWM). The apex of this was June 2022’s “Game On” initiative: UWM unilaterally slashed rates by 50-100 bps across all loans[3], turning the wholesale pricing landscape upside-down. Competitors complained that UWM was effectively doing loans at near-zero profit to drive them out. Indeed, UWM’s gain-on-sale margins in the second half of 2022 plunged (Q4 2022 margin was just 51 bps[72][73], versus ~100 bps prior to Game On). This move did capture massive market share - brokers, seeking the best deal for borrowers, funneled even more volume to UWM. Many rivals (e.g., Homepoint) couldn’t sustain the low margins and exited. By 2023, with fewer competitors standing, UWM gradually normalized pricing; full-year 2023 gain margin recovered to 92 bps[74][75], and by full-year 2024 it was ~110 bps, a 19% increase[76]. This shows UWM can flex pricing to offense or defense as needed. The question is: how sustainable is this advantage? In wholesale, price leadership is somewhat self-reinforcing - if UWM’s cost structure is lowest, it can offer lowest rates and still stay solvent, whereas higher-cost rivals bleed out if they match. UWM, by virtue of scale (handling $100B+ annually on one campus), likely does have the lowest cost per loan in the industry. That is part of its moat: smaller lenders simply cannot drop to UWM’s pricing for long because they lack similar economies of scale or low funding costs.

However, pricing power in a positive sense (i.e., the ability to raise margins) is limited. Mortgages are commoditized products; brokers will deliver loans to whoever offers the best combo of rate and service. UWM can’t gouge on price or brokers would shift volume (especially now that the #2 player in wholesale - Rocket Pro TPO - is backed by deep pockets and eager to regain share). Thus, UWM’s strategy is more about cost leadership than margin expansion. We expect margin sustainability around 0.9%-1.2% in normal environments. In boom times with constrained capacity (like 2020), margins industry-wide balloon (UWM’s peaked around ~200-300 bps in 2020). But competition inevitably brings them down. The encouraging sign is that UWM’s margins have stabilized and even risen slightly in late 2023/2024 while maintaining volume, implying some rationality returning as the weakest hands left the game. UWM’s recent guidance has typically bracketed ~75-100 bps in tough quarters and 100+ bps in better quarters[77]. We see limited upside beyond ~120 bps unless a refi boom lets everyone earn supernormal spreads before competitors catch up.

Moat Durability of Broker Channel Share: A core bet on UWM is a bet that the broker channel’s resurgence is durable. UWM argues that wholesale could grow from ~20% to 30% of the market over time[37][78], as more consumers realize they get better deals via brokers (and as more retail LOs switch to the broker model). There is logic to this: brokers can shop among lenders, potentially finding lower rates than a single retail lender’s offering. Plus, brokers thrived in the 1990s-2000s when they exceeded 30% market share - it’s not unprecedented. If wholesale does expand, UWM as the dominant player will benefit disproportionately. For instance, UWM illustrated that if it holds ~40% share of wholesale and wholesale grows from 20% to 30% of the market, UWM’s overall market share would jump from ~8% to ~12%[79][78] of all mortgages - a huge gain without needing other channels. Are there headwinds to this scenario? One risk is bank retrenchment could reverse - if big banks like Chase or Wells decide to re-enter wholesale or expand again, they could slow broker growth by keeping loans in-house. Another risk is consumer direct fintech platforms that bypass brokers (e.g., Better.com or Zillow Home Loans trying to create an online marketplace). To date, those have not meaningfully dented the broker model - many borrowers still prefer a human advisor, especially for home purchase transactions. Brokers offer personalized service that a call-center rep or purely digital interface often can’t. Additionally, regulations like RESPA prevent easily paying referral fees to realtors, which keeps brokers relevant as the local referral partner. We judge UWM’s moat in brokers as solid for now, but we watch for any sign of disintermediation.

Disintermediation Risks: Key competitive threats include:

Banks: Large banks historically had advantages like low-cost deposit funding and cross-sell, but they’ve lost mortgage market share (combined, banks now <30% of originations). Could they take back share? Possibly via portfolio lending (e.g., jumbos for affluent clients) or special programs (Chase using First Republic’s jumbo business). But banks face higher capital costs and regulatory scrutiny, and many seem content focusing on existing customers. Banks also largely shun brokers (few banks operate in wholesale now), so their competitive influence is mostly in retail and correspondent. UWM’s broker-centric model isn’t directly challenged by banks unless banks lure brokers to become retail LOs - which is hard since banks often pay less and have more bureaucracy.

Fintech/Direct Lenders: The likes of Rocket, loanDepot, Better, etc., invest heavily in consumer marketing and slick online apps. They aim to make getting a mortgage as easy as a few clicks, theoretically rendering a human broker less necessary. Rocket, for one, touts its “Rocket Mortgage” online approval. However, paradoxically Rocket has also launched a broker channel (Rocket Pro TPO), effectively acknowledging brokers won’t disappear. Fintechs have struggled to fully automate the mortgage (Still need appraisals, etc.). For many borrowers, especially first-timers, guidance on loan options is valuable - that’s the broker’s role.

Competitors in Wholesale: Rocket is the main competitor in the broker channel. Other notable wholesale lenders include PennyMac’s broker division, AmeriHome (owned by Western Alliance Bancorp), loanDepot’s wholesale arm (though loanDepot scaled back wholesale in 2022), and a number of mid-size players (Homepoint was #3 but exited; Freedom Mortgage does some wholesale mainly for VA loans). CrossCountry Mortgage, now a top-3 overall lender, is primarily retail but has been recruiting branches (some effectively operate like brokers). For UWM, Rocket Pro TPO is the most formidable: Rocket has brand recognition that brokers can leverage with clients, and Rocket can afford to price aggressively too (though Rocket’s strategy has been to keep margins high on consumer-direct while using wholesale to incrementally supplement volume). In 2020-21, Rocket tried to grow TPO but was still far behind UWM (Rocket’s wholesale share was ~10-15% versus UWM 35%+[80]). We expect Rocket to remain in wholesale as a thorn - interestingly, UWM’s broker ultimatum (banning brokers who used Rocket) actually indicates UWM viewed Rocket’s presence as a serious threat in 2021[25]. Legal and PR blowback forced UWM to soften that stance somewhat, but many brokers did choose sides. Today, some brokers are “loyal” to UWM, others send both UWM and Rocket (and others). UWM’s continued high share suggests Rocket hasn’t made huge inroads yet, but this rivalry will continue to shape pricing and service.

Pricing & Margins: The biggest risk to UWM’s moat might simply be a scenario where competitors engage in protracted price undercutting (a war of attrition). If a well-funded competitor decided to lose money for multiple years to gain share (effectively what UWM itself did to some extent in 2022), it could pressure UWM’s margins. Rocket, with its diversified business lines and large cash stockpile, could attempt this. However, Rocket has investors too and has thus far been reluctant to take its gain-on-sale margins as low as UWM’s wholesale rates - Rocket’s overall GOS was 2.80% in Q2 2025[81], far higher than UWM’s ~1.13%, indicating Rocket chooses to keep pricing higher and accept lower volume. UWM can thus leverage being a pure-play low-cost provider. Its lean operation (single location, no retail branches, highly automated) likely gives it a cost per loan that competitors can’t easily match without structural changes.

As long as the broker channel remains a viable and growing distribution path, UWM’s quasi-monopoly within that channel gives it a defensible franchise.

5. Funding & Capital Markets

The mortgage origination business is capital-intensive and depends on continuous liquidity to fund loans. UWM, like other non-bank lenders, doesn’t hold loans long-term - it originates to distribute. This model requires robust warehouse funding, adept interest rate risk management, and access to investors to purchase loans or securities. We examine UWM’s funding sources, liquidity position, and capital market activities:

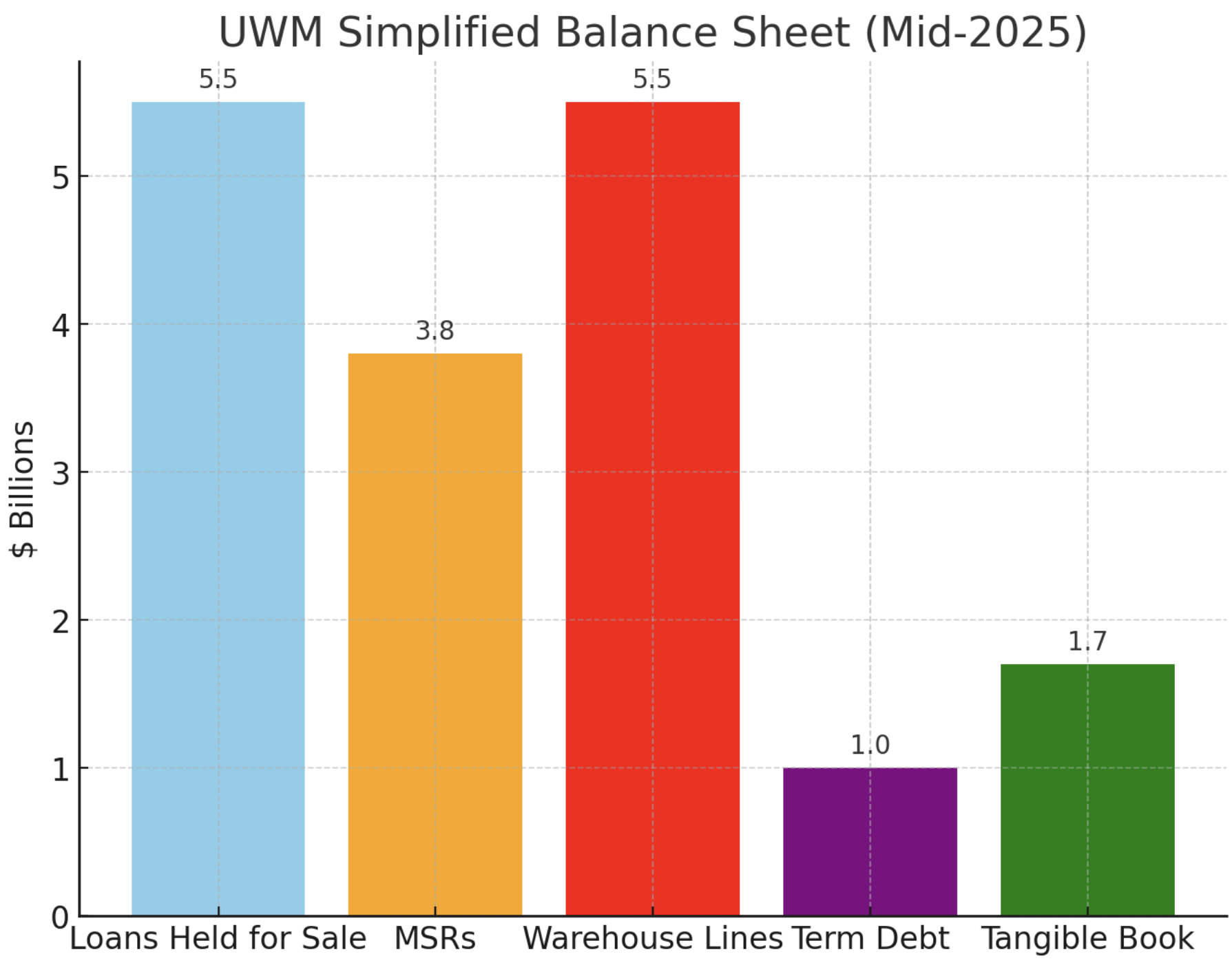

Warehouse Lines & Liquidity: UWM funds nearly all new loans by drawing on short-term warehouse credit lines from banks and financial counterparties. These are essentially large revolving facilities secured by the mortgages until they’re sold. As of the latest filings, UWM had multiple warehouse lines with a total capacity in the tens of billions (exact figures fluctuate; often it’s $20-30B+ across all lines). Utilization depends on loan volume at a given time. For instance, at Q3 2023, UWM had $5.56B of loans held for sale on its balance sheet[82][83], supported by warehouse borrowing (classified as funding debt) of similar magnitude. UWM’s counterparties for these lines include major global banks and possibly specialty finance firms. Historically, names like Bank of America, Barclays, Credit Suisse (before its demise), and smaller players like Texas Capital Bancshares have been active in warehouse lending to the industry. UWM has indicated confidence in its ability to tap and increase warehouse lines as needed[84][85], a reflection of its standing as the #1 originator - banks want to lend to those who will reliably generate fees and interest.

Warehouse lines typically fund around 98% of the loan value (with UWM posting the 2% equity “haircut” per loan). Interest on these lines is tied to short-term benchmarks (often 1-month SOFR/LIBOR + a spread). With the Fed’s hikes, UWM’s warehouse interest expense rose, but crucially, UWM only holds loans for a brief period (turnover in weeks). It hedges interest rate risk (discussed below) and generally passes through the cost via loan pricing. The risk is if a sudden liquidity crunch or credit event caused banks to cut these lines or issue a margin call (e.g., if the collateral value falls). We saw a mini-stress test in March 2020 when COVID froze the MBS market, and some non-banks faced margin calls on warehouse lines due to valuation marks. UWM navigated that period and since then has had a very strong capital buffer. As of Q2 2025, UWM had ~$2.2B of available liquidity (cash + undrawn lines)[27][28]. Specifically, ~$490M was cash on hand, and the rest was undrawn capacity on financing facilities. This liquidity provides a cushion to meet any margin calls or funding hiccups. Additionally, UWM has an unused revolving credit facility (corporate line separate from loan warehouses) for general liquidity, and it has specialized MSR lines which allow it to borrow against the value of its mortgage servicing rights. The Q2 2025 Rocket disclosure shows Rocket had $2.0B of undrawn MSR lines[86][87]; UWM likely has something comparable albeit smaller relative to its MSR value.

Secondary Market Execution - Loan Sales & Securitization: Once UWM closes a loan, it needs to sell or securitize it to repay the warehouse draw. UWM primarily utilizes two avenues:

Direct sales to the GSEs: For conforming loans (meeting Fannie Mae/Freddie Mac standards), UWM often takes the path of least resistance: selling the loans to Fannie/Freddie and retaining servicing. The GSEs will either package them into Agency MBS or hold temporarily. UWM gets paid a cash price that reflects the MBS value plus a servicing valuation. This is a quick, low-risk execution since the GSEs guarantee the credit risk.

Ginnie Mae securitization: UWM is an approved Ginnie Mae issuer, so it can pool FHA, VA, USDA loans into Ginnie Mae MBS. Ginnie Mae doesn’t buy loans; it guarantees the securities. So UWM actually issues the MBS itself (or through aggregation). It then sells these Ginnie MBS in the bond market. This process is a bit more involved but standard practice for government loans. UWM must manage the timeline and ensure investors buy the bonds. - Private whole loan sales or securitization: For loans that are non-agency (jumbo, non-QM), UWM finds third-party investors or aggregates for private label securitization. In 2021 it did a few private securitizations of jumbo loans (as did Rocket), but in the current market, demand for private MBS is lower. Most of UWM’s jumbos or non-QM likely are sold as whole loans to investors like banks, REITs, or asset managers. These sales carry some credit risk until sold and often at a slight discount to par (since no government guarantee). They are a small piece of UWM’s mix (about 11% of 2024 volume was non-agency[19]).

UWM’s gain-on-sale margins reflect how well it executes these sales. A higher margin can mean either selling at better prices or capturing more profit from high borrower rates relative to market rates. UWM hedges its interest rate exposure from the moment a loan rate is locked until sale (using MBS forward contracts, etc.). The goal is to lock in the spread. As long as UWM hedges effectively, short-term rate swings won’t materially hurt its sale execution. (The big GAAP losses we saw in some quarters were from MSR revaluations, not loan sale losses - in fact, UWM remained “operationally profitable” on loan production even when MSRs caused net losses[90][91].)

One area UWM has not significantly utilized is credit risk transfer (CRT). Some mortgage companies structure deals to offload credit risk (especially on jumbo or non-QM pools, via structured notes). UWM mostly sticks to selling to end buyers or doing whole loans. The GSEs themselves handle CRT via their CAS/STACR programs (doesn’t involve UWM directly). If GSE reform advanced where guarantors require originators to hold some risk, UWM might have to engage in CRT transactions then.

Mortgage Servicing Rights (MSR) Strategy: MSRs are a critical asset for UWM. Every loan UWM sells with servicing retained creates an MSR on its balance sheet, which is essentially the present value of future servicing fees. At Dec 31, 2023, UWM’s MSR asset was valued at $4.35B (for $299.5B UPB)[92][93]. By mid-2025, UPB was $211B with WAC 5.51%[27][94]. The large drop in UPB suggests UWM sold a chunk of MSRs in early 2024, or transferred some servicing. It’s known that UWM executed bulk MSR sales historically when it needed to manage cash or risk - for example, in 2022 it bought some MSRs from other lenders (Homepoint’s Ginnie MSRs), then later it may have sold some Agency MSRs when valuations were high. UWM likely opportunistically harvests MSR value: when rates rise, MSR values go up (because prepayments slow, extending the fee stream), which helped UWM in 2022 (they recorded fair value gains in some quarters, and sold $aspects to generate cash). Conversely, when rates fall, MSRs lose value (expected prepayment speeds jump). UWM’s hedging of MSR risk is limited - it typically takes GAAP hits as in Q4 2023 ($634M MSR value decline)[95][96]. But economically, falling rates would spur refis which boost originations, offsetting MSR losses with production income - a natural hedge.

The MSR sales provide liquidity: selling a portion of the servicing book can free hundreds of millions in cash, albeit at the cost of forfeiting future fee income. UWM did end 2023 with lower equity partly due to a huge MSR markdown; then in Q1 2024 it likely completed a sale (explaining the big UPB drop by mid-2024). In Q2 2025, UWM’s MSR was $211B UPB, $5.51% WAC[27] - comparatively high WAC means recent loans at high rates (valuable MSRs that won’t prepay until rates drop meaningfully). We view UWM’s MSR as a liquidity lever: it can always monetize servicing if it needs cash or if it wants to de-risk ahead of a refi wave. Many investors also like UWM for its MSR portfolio - which provides stable earnings in a rising rate world (in 2022, MSR revenues cushioned earnings when origination revenue collapsed). However, MSRs come with responsibilities: advancing payments for delinquent loans, maintaining compliance, etc. So far UWM has handled servicing well (its delinquency is below industry average: 1.09% 60+ day delinquency vs 1.53% industry[97][98]). If we saw credit deterioration (higher defaults), UWM might need to advance more cash on MSRs (which is another reason to have MSR lines).

Balance Sheet & Capital Allocation: UWM’s balance sheet is relatively straightforward for a non-bank: mostly loans held for sale (short-term), MSRs (long-term asset), and liabilities of warehouse lines and some term debt. The company’s tangible book value at 6/30/2025 was about $1.7B[99]. However, the market cap (including Class D shares at market price) is much higher - around $10.8B implied[100]. This discrepancy is because MSRs and other intangibles mean price-to-tangible book is elevated, and investors value UWM on earnings power rather than book. It’s not unusual; Rocket also trades above book due to its MSR.

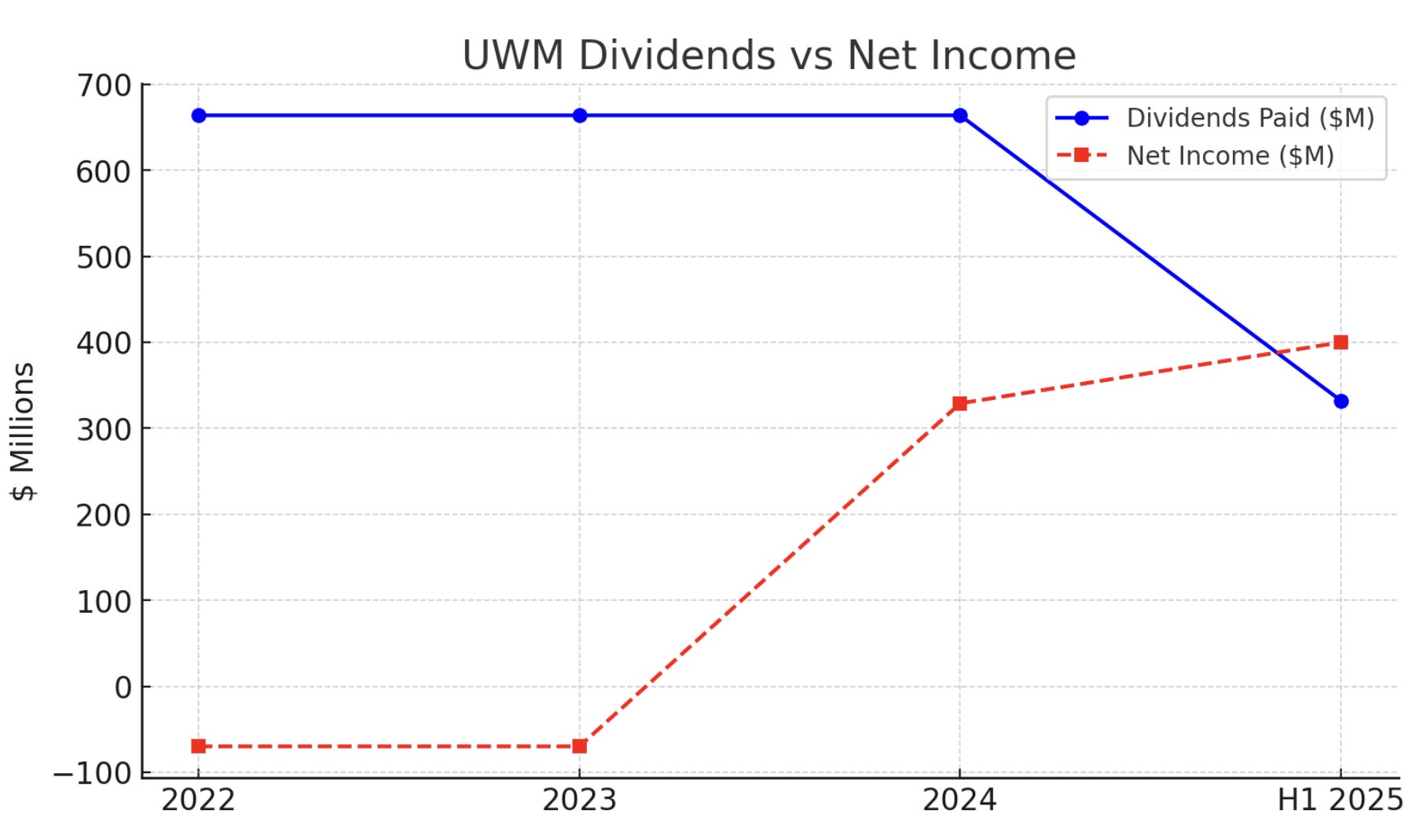

Capital allocation for UWM has been focused on dividends. The company committed to a $0.10/quarter dividend from its listing and has maintained it through ups and downs[7]. This yields ~6% annually at current stock prices - quite high. The dividend costs roughly $22M per quarter paid to Class A, but note that because of the Up-C structure, an equivalent distribution is paid to Class D (Ishbia’s entity) of around ~$144M per quarter[24] (since they own ~87% of total shares). So total cash outlay is ~$166M/quarter or $664M/year for dividends. This is substantial relative to earnings, and indeed in 2022-2023 UWM paid dividends even when GAAP net income was negative (they had positive operating cash flow though, and some historical profits to distribute). The Ishbias likely favored keeping this dividend to reward themselves and outside shareholders and to present UWMC as a yield play. We should scrutinize dividend sustainability: In 2023, UWM’s net loss was $70M, but adding back the non-cash MSR writedowns they had positive operating profit to cover the dividend (full-year adjusted net income was actually $490M before MSR marks[101]). In 2024, net income was $329M[23] which covers about half the $664M dividend; but UWM also had a large DTA shield (so minimal taxes) and some other adjustments, plus presumably some cash from MSR sales. As of mid-2025, with profitability restored (H1 2025 net income was substantial given Q2 alone $314M), the dividend seems secure in the short run. The company has not done share buybacks, probably because float is already small and Mat Ishbia doesn’t want to reduce it further (or use cash that way). No significant M&A has been done either (they prefer organic growth; they did buy some small tech assets but nothing major).

Looking at debt market access: UWM issued a 5.50% $700M 5-year senior unsecured bond in 2021 (due 2026) and a 5.75% $500M bond due 2027. Those rates were low at the time. Those bonds likely trade at yields above 5.5% now due to higher rates and sector spread, but UWM’s credit profile remains solid (no history of defaults, strong market position). If needed, UWM could raise debt again (albeit at higher coupons, probably high-single-digit yields today). Equity raises are unlikely given the structure - any new equity would have to come with Mat converting some of his interest, which he hasn’t shown inclination to do (and stock price in single digits is likely lower than what he’d accept for dilution).

Finally, one must consider risk management: UWM’s capital markets team manages pipeline hedging and MSR hedging. They appear to have done reasonably well - we haven’t heard of any hedging fiasco (unlike some lenders that got caught by rate spikes in 2020). They likely use forward MBS trades to hedge interest rate locks and use interest rate swaps or Treasuries to partially hedge MSRs (though MSR hedging is tricky and expensive, and UWM might just live with the volatility).

6. Financial Deep Dive

We now delve into UWM’s financial performance, focusing on recent results, key trends in revenues and margins, servicing metrics, and balance sheet health. We also compare UWM’s financial ratios to its closest peer, Rocket Companies (RKT), to contextualize valuation.

Revenue and Profitability Trends: UWM’s revenues are predominantly from loan production (gain-on-sale) and loan servicing. During the 2020-2021 boom, UWM’s financials swelled dramatically - 2021 net income was over $1 billion (helped by extraordinary refi volumes and wide margins). However, the subsequent downturn saw revenue fall and earnings compress:

2022: Volume fell and margins tightened significantly (especially after mid-2022’s price war). UWM remained profitable for part of 2022 but saw sharp declines. Full-year 2022 ended with a small net income on an adjusted basis, but GAAP was affected by fair value swings.

2023: Total originations were $108.3B[102][103], down about 16% from 2022’s $128.8B[104][105], yet UWM still achieved slight growth in purchase volume and increased overall market share. Full-year 2023 financials: Net loss of $69.8M[95], but this was after a massive $854M negative MSR valuation adjustment[95]. Excluding that, operating profit was positive. In fact, UWM touted that it was “operationally profitable” in 2023 despite the headline loss[106]. Revenue (total gain-on-sale plus servicing income) roughly tracked volume - Q4 2023 revenue was $302M[107] (very low due to MSR mark), whereas Q3 2023 was higher with an MSR mark-up. Gain-on-sale margin for full-year 2023 averaged 0.92%[108]. That represented margin compression from prior years but was a recovery from the ~0.5% trough in late 2022[72][109].

2024: A rebound year. UWM’s total originations jumped to $139.4B[110] (up 29% YoY from 2023’s $108B). Purchase volume hit a record $94B in 2024[111][112]. Importantly, gain-on-sale margins improved to around 1.10% for full-year 2024 (19% higher than 2023’s 92 bps)[76]. This was due to easing competitive pressure and higher average loan rates which can slightly boost gain on sale (with wider spreads on coupons). UWM’s GAAP net income for 2024 was reported as $329.4M[23] - a big swing back into the black. However, only $14.4M of that was attributable to Class A shareholders[113] due to the structure; the rest was non-controlling interest (Mat’s share).

LTM (Latest Twelve Months): If we take Q3 2024 through Q2 2025 as LTM, UWM’s volume would be roughly ~$140B (since Q3 & Q4 2024 plus Q1 & Q2 2025 were all in the $25-40B range each). LTM revenue (excluding MSR marks) likely around $2.5B. LTM net income is harder to compute from external sources, but given Q3 2024 had net income ~$300M, Q4 2024 maybe around breakeven (with some MSR hit), Q1 2025 was a large loss of $247M[114], and Q2 2025 big profit $314.5M[115], the net of those four quarters is still positive (roughly $+150M). Adjusted for MSR noise, the core earnings power LTM is higher.

Recent Quarter (2Q 2025) Highlights: UWM’s Q2 2025 results underscore improving trends: - Originations $39.7B, up 18% YoY[115][6]. - Total revenue $759M and net income $314.5M[116][117]. Notably, net income margin was ~41% of revenue, reflecting significant MSR mark-to-market gains in that quarter as rates rose (slowing prepayments). - Gain-on-sale margin 113 bps, up from 106 bps in 2Q24[6]. - UWM’s cost-to-produce (expenses) are not directly broken out here, but one can infer: At 113 bps margin on $39.7B, production revenue was ~$449M. Net income $314M after some mark-ups implies expenses plus interest in Q2 were maybe ~$200-250M range. UWM’s expense structure (compensation, facilities, etc.) has been rightsized with some layoffs in 2022, but they emphasize not cutting too deep to handle future volume.

Expense Management: UWM’s main operating expenses are personnel (thousands of underwriters, ops staff), marketing, tech, and general overhead. It does not have commissions to a salesforce (brokers are independent and get paid via fees on loans, not by UWM). During lean times, UWM has prided itself on not doing mass layoffs (unlike Rocket which cut thousands). However, UWM did reduce staffing from ~8,000 at peak to ~6,000-7,000 now through attrition and performance management. The expense base in 2023 was around $1.1B (total expenses)[118][119]. Rocket’s total expenses were higher ($1.336B in Q2 25 alone)[118]. UWM’s leaner cost per loan is a differentiator - in Q2 2025, expense per loan was roughly $200M / 146k loans ~ $1,370 per loan, whereas many lenders are $4-6k per loan in costs. (These rough calculations highlight UWM’s efficiency.)

Gain-on-Sale Margin Dynamics: The gain-on-sale (GOS) margin is a critical profitability metric for mortgage lenders. UWM’s GOS margin history:

2020: ~300+ bps (industry capacity crunch).

2021: around 100-150 bps as competition normalized.

2022: started ~80-100 bps, fell to ~50 bps by Q4 22 due to Game On.

2023: rebounded to ~75-100 bps range each quarter, averaging 92 bps[108].

2024: climbed into 100-120 bps range as pricing rationalized.

2025 Q1: 94 bps.

2025 Q2: 113 bps[6].

We see that margin compression hit hardest in late 2022 when UWM forced prices down. The trend now is moderate expansion as volumes recover and fewer competitors remain. However, we caution that if a refi boom hits, many lenders may re-enter or new ones form, potentially putting a ceiling on margins after an initial surge. UWM guides conservatively; for Q3 2025 they expected 85-110 bps[77]. We believe 100 bps is a reasonable run-rate in the near term, with upside if volume stress eases pricing, and downside if a new price war ignites.

Servicing Portfolio & MSR Sensitivity: UWM’s servicing portfolio (loans it services for others) generates fee income recorded in “Loan servicing and other” revenue. In 2024, servicing fees were on the order of $700+ million (since $300B average UPB * ~0.25% base servicing fee = $750M). However, GAAP servicing net revenue is impacted by MSR amortization and mark-to-market changes. For instance, when rates rose in Q3 2023, UWM likely recorded MSR fair value gains (contributing to the $301M profit that quarter[73]), whereas when rates fell in Q4 2023, they marked down MSRs $634M, causing a loss[95]. UWM does report an adjusted metric excluding “Assumption changes” in MSR values. Removing those volatile items, UWM’s servicing EBITDA is quite stable - the cash flow from servicing (fees minus costs to service) is largely recurring.

The MSR asset’s sensitivity: A rule of thumb is that a 1 percentage point decline in mortgage rates can reduce MSR value by 20-30%. Conversely, a rate spike increases MSR value similarly. UWM’s MSR had a weighted average coupon of 4.43% at end of 2023[92]. By mid-2025, WAC 5.51%[27] means lots of high-rate loans that won’t refi until rates drop below ~5%. If the Fed cuts and 30-year rates go from ~7% to, say, 5%, a large chunk of those 5.5% WAC loans become refi candidates, implying MSR runoff will accelerate (prepayments). UWM would mark down MSRs accordingly - possibly a hit of several hundred million on the asset. This is not a cash loss per se (just future fees coming off the books), and it would be offset by increased origination income as those loans refinance (likely through UWM again via brokers). Nonetheless, such accounting swings can whiplash earnings quarter to quarter. The market may look through it; indeed in 2023 investors seemed to ignore the GAAP loss, focusing on the core operations. For prudence, we expect UWM to perhaps sell MSRs proactively if a refi wave looms. They could convert some MSRs to cash at current high valuations to both lock in gains and reduce exposure.

Leverage and Debt: We touched on warehouse facilities earlier. On longer-term debt, UWM’s $1.2B of senior unsecured notes (5.5% and 5.75% coupons) are due in 2026 and 2027. These are modest relative to cash flow, but refinancing them will come at higher rates. By 2026, presumably credit markets normalize; UWM might pay them off with cash (if profitability stays high) or roll them. UWM’s debt-to-equity was ~1.0x at end of 2022, crept up to 1.5x in 2023 due to equity falling from MSR markdowns, and is about 1.0x again after Q2 2025’s profit restored equity to $1.7B. We don’t find this leverage concerning given the asset (MSRs) and the nature of the business (highly cash-generative in normal conditions).

Dividend Sustainability: We should re-emphasize that the $0.40 annual dividend ($0.10 quarterly) equates to roughly $640M/year for all shares (A + D). Can UWM’s cash flows support this? In 2021, absolutely (they earned far more than that). In 2022, they actually borrowed $500M via bond partly to fund operations and still paid the dividend - effectively using debt or balance sheet to fund payout during lean times, which is a bit concerning if prolonged. 2023’s operating cash flow was positive enough to cover because, while GAAP net was a loss, depreciation plus MSR changes are non-cash. Indeed, UWM’s operating cash flow in 2023 was +$1.5B, largely by shrinking loans held (releasing cash) and selling MSRs, whereas free cash flow after loan fundings is not a very useful metric given the working capital swings. We think management is committed to the dividend unless a severe liquidity crunch occurs. It’s part of their thesis to investors that UWMC is a yield play with upside.

Cash Flow vs Accounting Earnings: Mortgage companies often have divergent cash vs earnings. UWM’s cash flow from operations tends to be lumpy: in periods of growth, it uses cash to fund more loans (temporary outflow), in slow periods it recoups cash as loans runoff/sold. UWM also has significant tax savings due to its Up-C structure: it can deduct certain payments to the Ishbia-owned LLC (and Ishbia pays taxes individually). There’s also a large deferred tax asset recorded with the SPAC deal that reduces cash taxes. So actual cash taxes paid are minimal currently, boosting cash flow. Meanwhile, GAAP earnings swing with unrealized MSR marks that have no immediate cash impact.

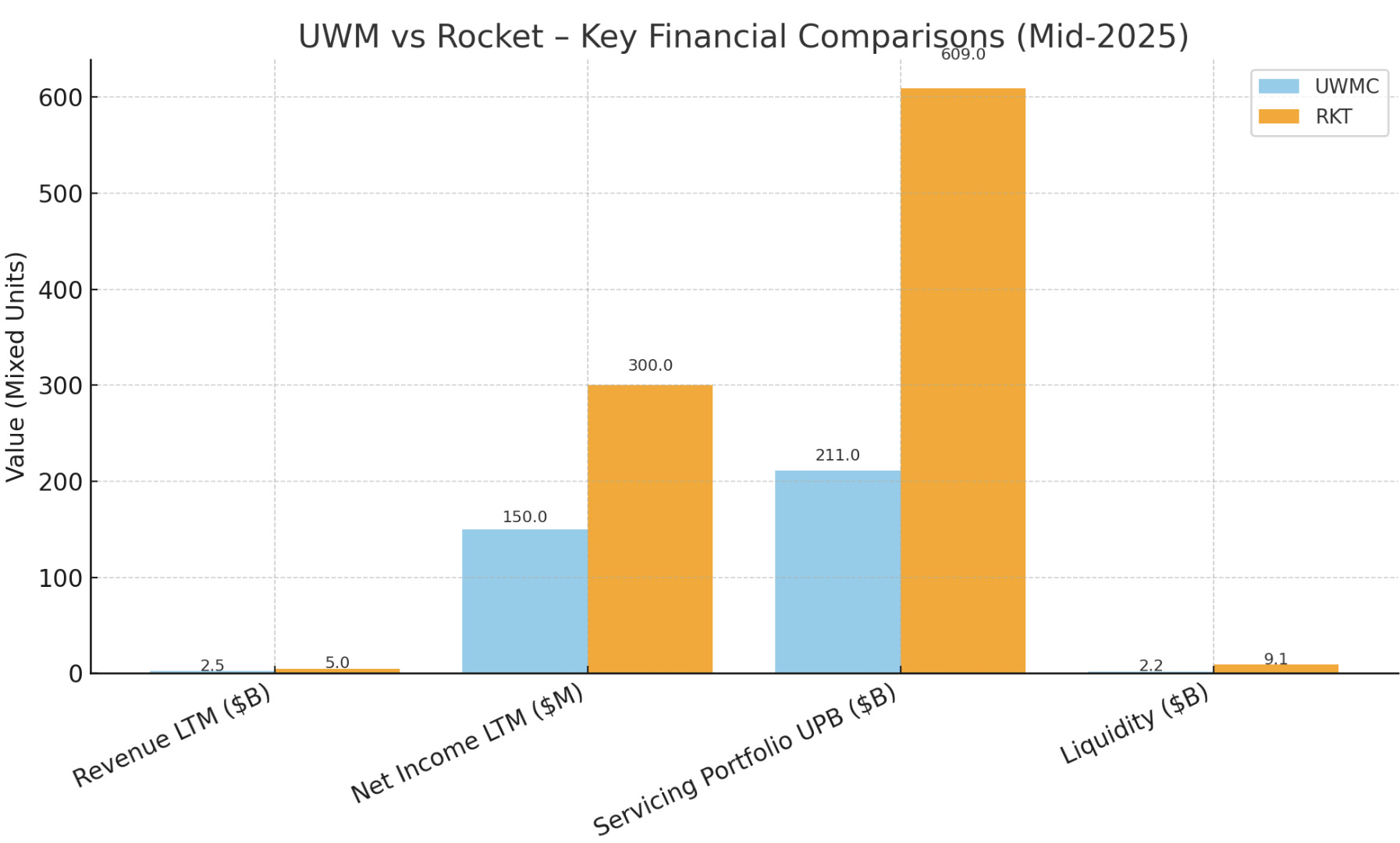

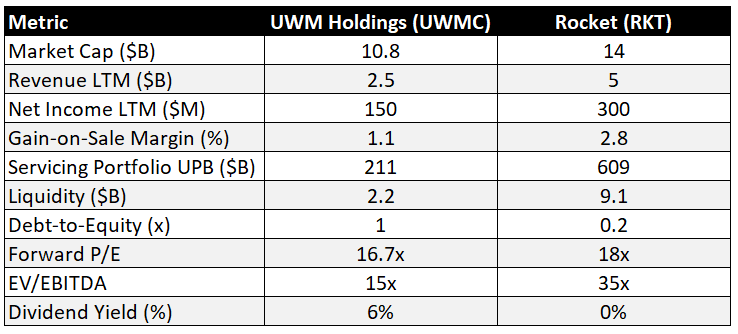

Peer Comparison (UWMC vs RKT): We compare UWM to Rocket (RKT), across key metrics (trailing figures as of mid-2025):

Market Cap: UWMC’s effective total market cap (including class D) is ~$10.8B[100], versus RKT’s market cap around $14B (RKT at ~$11/share with ~1.26B shares including Class D super-voting shares held by Dan Gilbert). However, the public float market cap is $1.5B for UWMC (only 13% of shares)[120][121], while RKT’s public float is larger since they IPO’d ~20% of shares and Gilbert since sold some.

Revenue (LTM): UWM LTM revenue ≈ $2.5B (est.), RKT LTM revenue (2024 + H1 2025) was ~$5.0B (Rocket generates more revenue per loan due to higher margins, plus has non-mortgage revenue streams like servicing fees on a bigger book and Rocket Homes etc.). In Q2 2025, Rocket’s revenue was $1.36B[122], nearly double UWM’s $759M[116], despite UWM writing more loan volume. This underscores the stark difference in gain-on-sale: Rocket’s 2.8% margin vs UWM’s ~1.1%[6][81].

Net Income (LTM): UWM LTM net ~$150M (adjusted for MSR). RKT had a GAAP net loss of -$178M for H1 2025 (and $469M profit 2024)[123], so trailing maybe ~$300M GAAP profit if we combine? Actually, RKT’s GAAP net in 2024 was boosted by a one-time gain from a subsidiary sale and big MSR marks. Core profitability at Rocket has been challenged; their Q2 2025 GAAP net was only $34M[124]. On an adjusted EBITDA basis, RKT had $172M in Q2 25[125] vs UWM $196M[126], surprisingly close.

Margins: UWM’s operating margin is slim in tough times but can exceed 50% in boom times (as minimal marginal cost on extra loans). Rocket’s operating margins are typically lower on volume because they spend heavily on marketing (~$100M per quarter in ads, which UWM doesn’t have as a B2B business). For example, RKT’s total expense in Q2 25 was $1.336B[119] on $1.36B revenue - essentially break-even before interest and taxes. UWM’s expense was maybe $450M on $759M revenue, leaving plenty of op profit. This indicates UWM’s lean model yields higher profitability at equivalent volumes, but RKT tries to compensate with higher revenue per loan.

Servicing Portfolio: UWM $211B UPB[27], RKT $609B (including subserviced)[127]. Rocket’s servicing book is ~3X UWM’s, which is a huge difference. That means Rocket gets a steadier large stream of servicing income ($609B * ~0.30% ≈ $1.8B gross annual fees) - which helped it stay afloat in 2022 when originations fell. UWM’s servicing fees (maybe ~$0.6B) are smaller but still significant relative to its revenue.

MSR Fair Value: On balance sheet, UWM MSR was ~$3.6B mid-2025 (implied from $211B at ~1.7% of UPB), Rocket’s MSR is larger. Both mark to market, but Rocket appears to hedge a portion or had less volatility (Rocket had a $200M MSR loss in Q2 25[128], while UWM had a $... actually UWM had a gain Q2 25 given net profit soared).

Leverage: UWM’s debt-to-equity ~1x, RKT is debt-light (they have about $2B corporate cash vs similar debt, effectively no net debt). Gilbert’s philosophy was to maintain fortress balance sheet, which they have - Rocket had $9.1B total liquidity including $5.9B cash as of Q2 25[129]. UWM’s liquidity $2.2B including $0.49B cash[27]. So Rocket has far more dry powder (they are using it to make acquisitions like Redfin’s mortgage arm and recently announced buying serviced loans from Mr. Cooper).

Valuation Multiples: - P/E: Trailing P/E for UWMC is very high (because trailing earnings were tiny). Yahoo Finance shows ~168x trailing[120], which is not meaningful. Forward P/E ~16.7x[120] implies analysts expect about $0.40 EPS next year (the stock ~$6.7). For RKT, trailing P/E is N/A or high as well (they had small profits), forward P/E likely high teens too (the street expects RKT to return to larger profits by 2025, but uncertain).

P/B: UWMC’s P/B is ~4x (with book equity $1.7B vs market cap $7B counting only A shares at market? But including Ishbia stake, P/B ~6x). Rocket’s P/B ~1.5x (Rocket’s equity ~ $8B vs $12B mkt cap).

P/Tangible Book: More relevant since goodwill not big here: similar to P/B because most of equity is tangible MSR asset.

EV/EBITDA: For mortgage companies, EBITDA is not a perfect measure due to mark-to-market. Using adjusted EBITDA: UWM’s 2024 adjusted EBITDA was $720M (approx), so EV/EBITDA ~15x. RKT’s 2024 adjusted EBITDA was $341M[130] (H1 2025 $341M, 2024 maybe ~$400M), EV/EBITDA higher around 35x. So UWM appears cheaper on that metric, but keep in mind UWM’s EBITDA excludes taxes that are avoided due to Up-C structure.

Dividend Yield: UWMC ~6% (and that yield is only on the Class A public shares; Ishbia’s portion isn’t publicly traded but he gets the cash - from a Class A investor perspective, 6% yield is real). RKT’s dividend yield is zero (Rocket doesn’t pay a regular dividend, they did a one-time special $1.01 in 2022 when flush with cash, but none recurring).

In summary of peer comp: UWM trades at a lower valuation relative to near-term earnings and pays a dividend, reflecting perhaps a “value”/income orientation, whereas Rocket is priced more as a “growth/tech” story (higher multiple, reinvesting cash into acquisitions and tech, no dividend). UWM’s financials show higher efficiency and current profitability; Rocket has a stronger liquidity buffer and diversification (e.g., Rocket’s new businesses like auto lending, personal loans via Rocket Money, real estate search via Redfin partnership). In Section 9, we will do a deeper qualitative comparison.

7. Macro & Policy Overlay

UWM’s fortunes are tightly intertwined with the macroeconomic environment, particularly interest rate trends, housing market conditions, and public policy shifts. In this section, we overlay the broader macro outlook and explore scenario implications:

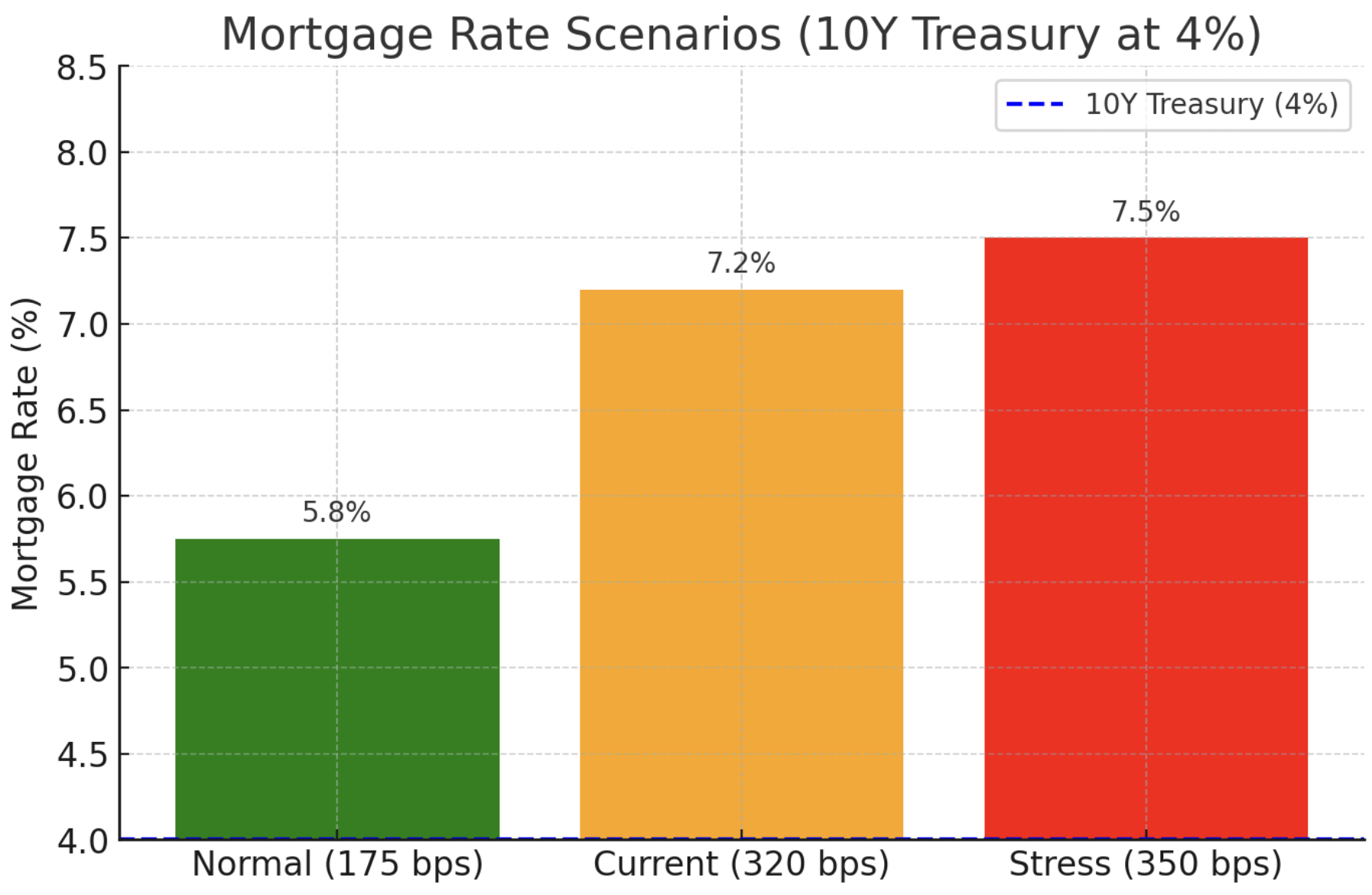

Federal Reserve Policy & Rate Path: After 2022’s aggressive tightening, the Fed in 2023-2024 held the federal funds rate in the ~5.25% range, which translated to 30-year mortgage rates oscillating between 6% and 8% (the highest sustained levels since 2000). As of late 2025, markets are anticipating that the Fed’s next moves will be rate cuts given cooling inflation and economic headwinds. A consensus expects perhaps 50-100 bps of cuts in 2024, barring any re-acceleration of inflation. For UWM, the timing and pace of Fed cuts is the single biggest catalyst. A gradual decline in mortgage rates from ~7% towards, say, 5% over the next 18 months would create a Goldilocks scenario: improved affordability (stimulating purchase demand) and a gradual reopening of refinance opportunities - but not so abruptly that capacity issues drive margins to zero. On the other hand, if cuts come very fast or unexpectedly large (e.g., a recession prompts the Fed to slash 200 bps in a short span), we could see a tsunami of refinances. While that boosts volume, it could actually compress margins initially (as every lender scrambles to capture refis, possibly resurrecting dormant competitors). Still, on balance a falling rate environment is positive for UWM’s business volume - the key is ensuring hedges are in place for the pipeline and MSRs.

If rates instead remain “higher for longer” - suppose inflation proves sticky and the Fed doesn’t cut or even hikes more - mortgage rates could stay ~7-8% through 2025. In that case, the purchase market likely remains tepid and refis negligible, implying the overall pie stays small. UWM would then rely on market share gains to grow (taking from others). They have shown the ability to do that, but incremental share gains get harder the larger they already are (they’re already #1). Under a stagnant high-rate scenario, we’d expect UWM to still be profitable (due to having scaled down costs to current volumes and benefiting from servicing income in high rates). But earnings growth would be muted, and the dividend would likely become the main shareholder return (with limited stock appreciation).

Mortgage Spreads: It’s not just Fed policy; the spread between mortgage rates and Treasuries is unusually wide right now (~300+ bps vs a more normal 150-200 bps). This is due to various factors: MBS market technicals (the Fed stopped buying MBS and is running off its portfolio), higher volatility, and credit/liquidity premiums. If macro uncertainty abates and the Fed or banks show interest in MBS again, spreads could tighten, meaning mortgage rates could fall even if the 10-year Treasury doesn’t fall as much. For instance, even if the 10-year stays at 4%, the mortgage rate could ease from 7.5% to 6% if the spread normalized. That would be hugely beneficial to originations. Conversely, in a stress scenario (e.g., another credit crunch or Fed balance sheet reduction), spreads could widen further, keeping mortgage rates elevated relative to benchmarks. UWM as an originator doesn’t directly control spreads, but it’s a factor to watch - narrower spreads typically improve gain-on-sale execution (higher prices for MBS).

Housing Affordability & Supply-Demand: Housing affordability is currently near multi-decade lows due to the combination of high home prices and high interest rates. The affordability index (median income vs median home payment) plummeted in 2022-23. This constrained many first-time buyers. However, there are cross-currents: Household formation is still positive (millennials aging into prime homebuying years, Gen Z coming up) which supports underlying demand. The issue is supply - the inventory of homes for sale is extremely low (many homeowners with low-rate mortgages are not selling, and new construction only partially fills the gap). This supply shortage has propped up home prices even in a high-rate environment (we haven’t seen a big price crash, just stagnation or slight dips in some markets). For UWM, stable to rising home prices are a double-edged sword: positive for collateral values (less credit risk, higher loan sizes) but negative for affordability/volume. The ideal scenario for UWM might be a modest national home price correction (say 5-10%) coupled with lower rates - this would revive transaction activity without causing borrower distress. However, absent a surge in supply, home prices might remain firm. If wages continue rising (the labor market is still relatively strong) and rates fall a bit, affordability can improve somewhat and unlock demand.

Another dynamic is rent vs buy: As rents have also soared, in some cases even a 7% mortgage can be as affordable as rent, pushing certain buyers to proceed despite rates. If a mild recession hits and rent inflation slows while rates remain high, some marginal buyers may pull back, delaying homeownership.

Fiscal and Political Factors: While not directly in UWM’s control, broad fiscal policy can influence housing. For example, any new first-time homebuyer tax credits or down payment assistance programs (which have been discussed in Congress) could stimulate purchase volume at the margin, especially for FHA loans (a segment UWM does a fair amount in through brokers). On the flip side, if fiscal gridlock or austerity measures contract government spending, the economy could slow more, reducing housing demand.

Tariffs and Inflation Inputs: The prompt mentioned tariffs, which likely refers to building material costs (tariffs on lumber or steel) - relevant to home construction. High construction costs and labor shortages have limited new home supply. If tariffs were lifted or supply chain improved, cheaper construction could lead to more housing starts, indirectly benefiting mortgage lenders by easing inventory pressures. It’s a minor lever but worth noting.

8. Market Sentiment & Positioning

Understanding how the market perceives UWMC - across sell-side analysts, institutional investors, retail traders, and even how the stock is positioned in derivatives markets - can offer insight into potential sentiment shifts or contrarian opportunities.

Sell-Side Analyst Coverage: UWM is followed by a modest number of analysts (around 7-8 on Wall Street)[135][136]. The current consensus rating skews neutral. Many analysts have been on the sidelines due to the tough industry conditions; the average rating is around “Hold.” Price targets average roughly $5.50-$6.50[137][138], which, notably, UWMC’s recent price around $6.70 already exceeds[138]. This suggests the sell-side has been behind the curve - possibly underestimating the earnings rebound. Indeed, one data point shows average target $5.97 while stock was ~$6.72[138], implying slight downside according to analysts. There’s a wide divergence: some have low targets ~$4.50 (likely reflecting bear case high-rate scenario)[139], while one or two optimistic calls go up to $10[140][141] (likely assuming rate cuts and refi boom in forecasts). A recent example: Keefe, Bruyette & Woods (KBW) had a $4.50 target as of July 2025[139], possibly expecting continued margin pressure, whereas others like JP Morgan or BTIG might be higher.

The sell-side narrative often frames UWMC as a market share leader but in a cyclical trough, with some caution on its multi-class share structure and the sustainability of the dividend. As 2024 progressed with improving results, we might see upgrades or target raises. Importantly, because UWMC has a small float and is controlled by insiders, some larger banks’ analysts may give it less attention than Rocket (which had the flashy fintech narrative in 2020 IPO). If the macro turn becomes evident (e.g., Fed signals cuts), analysts could pivot to more bullish stances quickly, and price targets could rerate upward significantly given operating leverage.

As of now, the buy-side seems generally underweight mortgage originators - many got burned by the rapid decline post-2021, and with so many other sectors to invest in, not many generalist funds are actively adding exposure here yet. This sets up potential for sentiment improvement if macro data supports housing (e.g., a few months of falling rates or rising home sales could bring funds back into the space).

Short Interest & Options Positioning: UWMC has a notable short interest. Roughly 35 million shares short as of the last report, which is only ~2% of total shares but nearly ~18-20% of the free float[142][31]. This high short percentage of float implies some investors possibly pair-trading (long Rocket, short UWM? or short as a hedge for MBS exposure) or simply betting against the company’s valuation/dividend sustainability. Historically, UWMC had episodes where shorts targeted it post-SPAC, thinking the valuation was too rich or the dividend unsustainable. Those shorts did get squeezed at times - e.g., in early 2021 the stock spiked from ~$7 to $12 in a short squeeze scenario when retail interest surged.

We also note that Mat Ishbia’s ownership concentration means the effective float is small, so any incremental institutional buying or selling has outsize impact on price. If, say, a large index fund or ETF (like a housing ETF or small-cap value fund) decided to increase allocation, it could move the stock. Similarly, if some large holders (maybe a Tiger Global type - just hypothetical, not sure if they hold) decided to exit, liquidity could be an issue and push the stock down.

9. The Big Question: UWMC vs Rocket (RKT)

United Wholesale Mortgage (UWMC) and Rocket Companies (RKT) have emerged as the two titans of the U.S. mortgage industry, but they operate with starkly contrasting business models. This section provides a head-to-head comparison across multiple dimensions:

Market Share & Channel Focus:

UWMC (UWM Holdings): Market share leader overall in 2023 and 2024[42][40], driven by dominance in the wholesale channel (brokered loans). In 2024, UWM originated ~$138 billion (11% share of all mortgages) compared to Rocket’s ~$92 billion[48][49]. UWM’s share of the broker segment was an astounding ~43.5% in 2024[1]. However, UWM has essentially zero presence in retail or direct lending. Its fate is tied to brokers, which accounted for 100% of its production.

Rocket: Long-time #1 lender from 2018-2021 until UWM overtook[40]. Rocket’s core is retail/consumer-direct via its Rocket Mortgage platform. It does loans nationwide through its online and call-center infrastructure. Rocket also has a wholesale channel called Rocket Pro TPO, but its share there is small (~6-7% of wholesale by some estimates)[80]. Rocket’s 2024 volume of $92B was split roughly $50B purchase, $40B refi[53][144] - it led in refis until 2024 where UWM slightly surpassed it[145]. Rocket’s reliance on refinances historically was higher; in 2020, refis were the bulk of its volume. It has been pushing to grow purchase share (aiming to double purchase share by 2027)[146], including via acquisitions like Redfin’s mortgage arm to feed purchase leads[147].

Business Model Contrast:

UWMC’s Broker-First Model: UWM’s customers are independent brokers, not the end borrowers. It does no consumer advertising; its “sales” are essentially the broker relations and account executives catering to brokers. This B2B model yields lower revenue per loan (because the broker takes a share of the fees and UWM offers low rates to win broker business) but also comes with lower costs (no retail branch overhead, no massive advertising spend). UWM’s approach is high-volume, low-margin, akin to a wholesale distributor in any industry. It focuses on providing the platform (underwriting, closing, servicing) efficiently at scale. Importantly, UWM cedes the customer relationship to brokers - that’s a risk if one believes controlling the customer is vital, but UWM bets that by empowering brokers it will get repeat business anyway. One might say UWM is “the lender behind the lenders,” content with being less visible to borrowers (many borrowers might not even recognize UWM’s name, seeing only their broker’s branding and then receiving a note that UWM is the loan servicer).