Shorting Palantir

Too expensive & chart looks extended

AD Fund Management LP crossed triple digits (net) as of October 2025, I am waiting for the NAV numbers to finalize to get the exact % amount. I’m extremely happy for obvious reasons as an investor.

PLTR 0.00%↑ has been the bane of my short selling track record in 2025 - I like the company, hate the stock. I feel like most investors would agree with me, I have been wrong since the beginning of this year and after earnings results tonight (11/3/2025) I doubled my position making PLTR 0.00%↑ the single largest short in the portfolio. I want the stock to cross below $175 before the year ends.

Thesis

Palantir is a serious software company with real impact in high-stakes environments, but the equity embeds a frictionless AI rollout and commercial inevitability that the contract math, sales motion, and competitive surface do not yet justify. PLTR 0.00%↑ is simply too expensive.

What Palantir actually does

Palantir sells a stack of decision software that connects governed data to live operations. Gotham sits in defense, intelligence, and public-safety missions to fuse messy, sensitive data and drive actions under tight constraints. Foundry and AIP carry that pattern into the enterprise: Foundry gives you data pipelines, governance, and applications; AIP is an AI platform that mounts LLMs and agents on top of governed data and workflows so teams can build automations that act, not just chat over documents. Apollo is the continuous delivery and control plane that lets Palantir ship, secure, and patch all of the above across cloud, on-prem, and air-gapped environments.

and custom AI products (Build with AIP).")

If you read the product documentation, you see a consistent architecture: AIP capabilities for building agents and automations on top of an ontology, Foundry’s platform backbone, and Apollo running the software supply chain into regulated environments. This is enterprise-grade kit designed for operational outcomes, not for ad-hoc dashboards. (Palantir)

Where investors (including myself) went wrong

The Street extrapolated cloud-style velocity and unit economics onto a deployment model that depends on organizational change. Palantir’s highest-value wins require senior sponsorship, process redesign, and risk-bearing governance embedded in core workflows. That is why the software can be defensible.

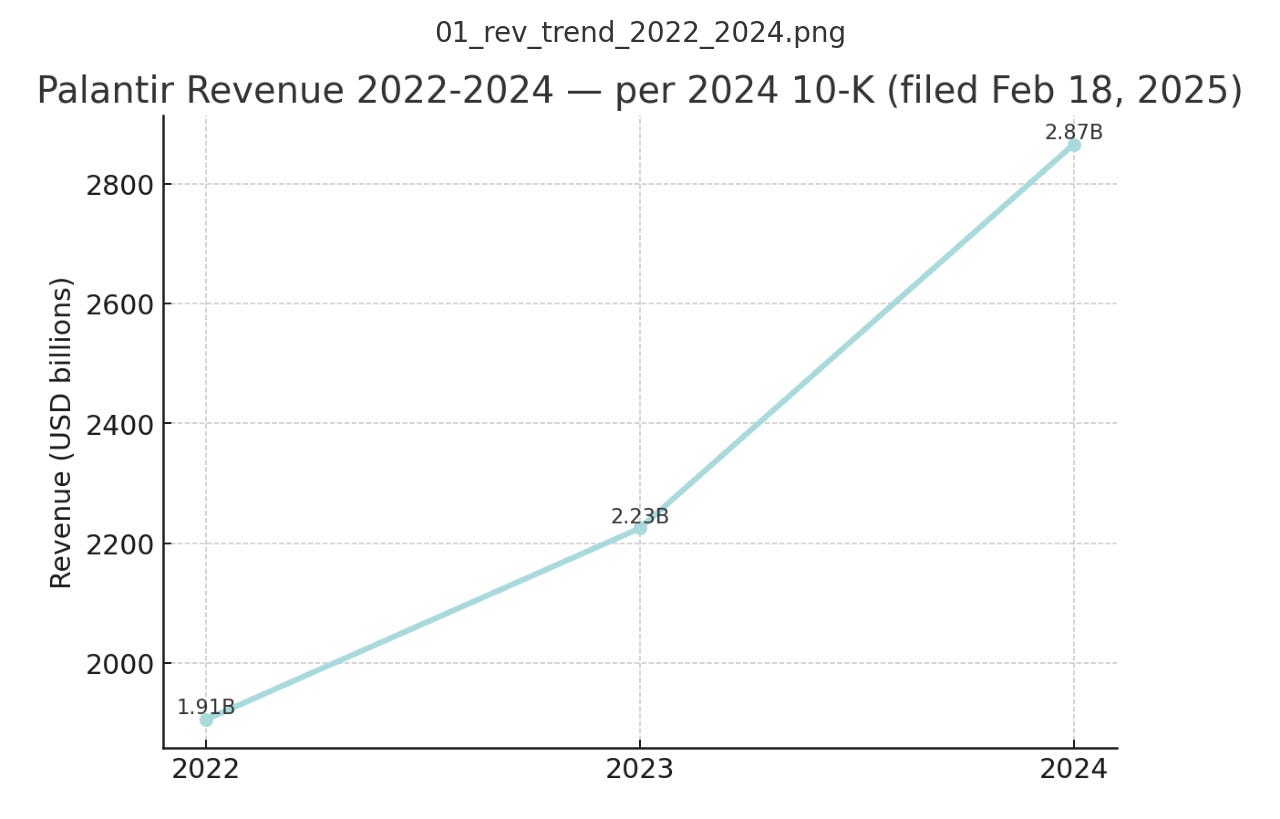

It is also why cycles are long, first waves are services-heavy, and bookings can be late-quarter and lumpy. The company’s own filings say as much, flagging elongated evaluations, customization, and the concentration and timing risks that come with large public-sector and blue-chip enterprise customers. Translate that plain language into equity terms and you get a revenue engine that compounds, but on a cadence closer to program rollouts than viral seat expansion. The short argument does not deny progress; it denies inevitability on the timeline the stock implies. The 2024 10-K lays out those risks in black and white. (Palantir Investors)

On Peter Thiel

I love this man - I think he is an absolute legend, and one of the few remaining original thinkers in Silicon Valley with big cojones. I admire Peter Thiel’s clarity on power laws, defensibility, and building for edge cases that matter. Palantir’s existence validates the idea that software can reshape national-security and industrial problems if you design for the hardest constraints first. Thiel, I believe, got burned selling META 0.00%↑ too early, and he convinced himself to hold onto his next big thing PLTR 0.00%↑ for dear life - the Thiel I studied would’ve exited 200% ago.

The world in which Palantir becomes the horizontally adopted AI operating layer across the median enterprise is a possible world; it is not the default path, and the burden of proof sits with the next several quarters of operating execution.

Tape and technical setup

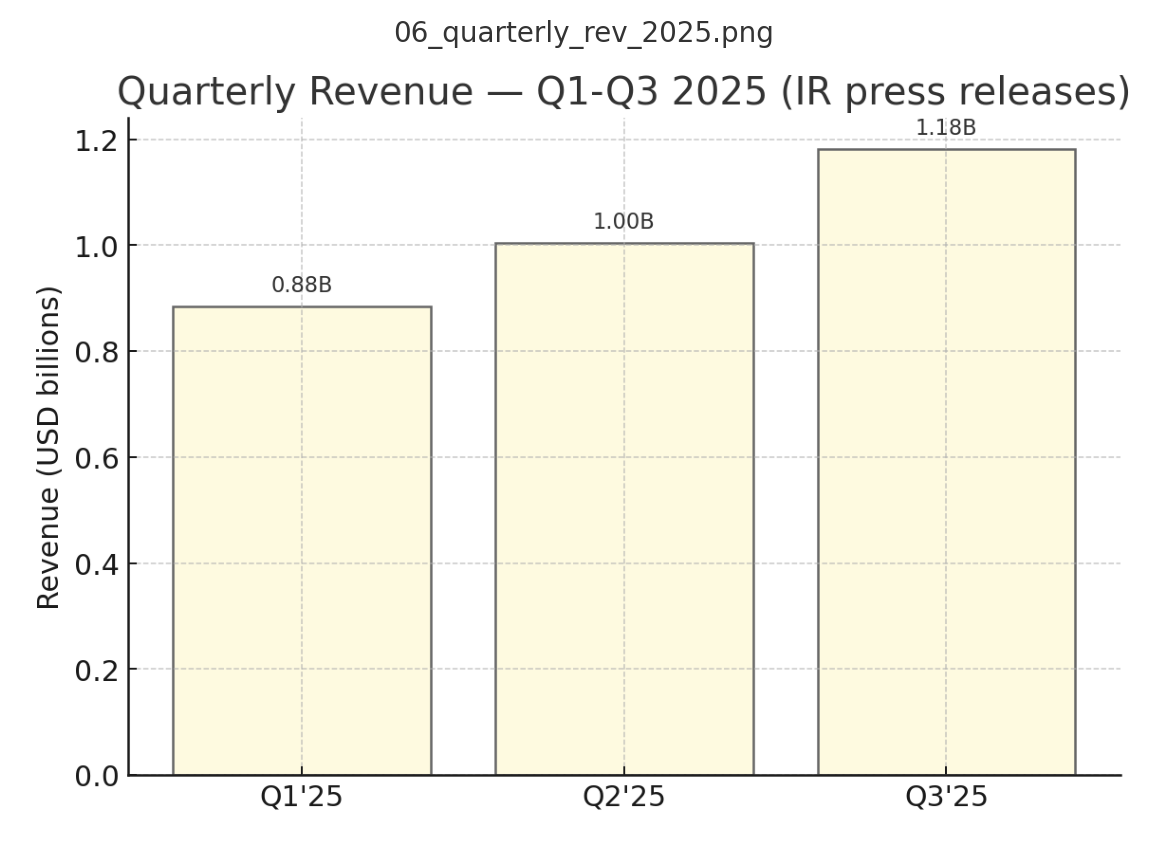

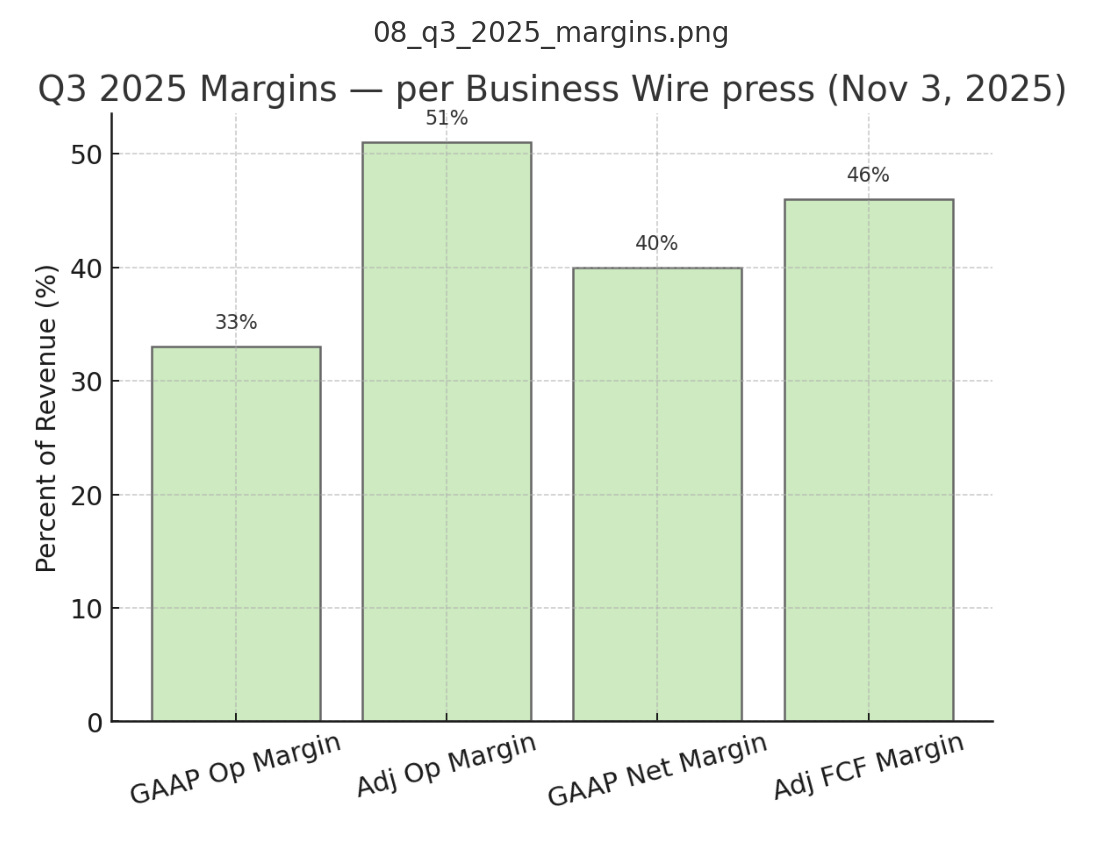

Q3 2025 was objectively strong. Revenue printed about $1.18Bn dollars, up 63% YoY, with U.S. commercial up roughly 121%, and management raised full-year revenue guidance to a $4.396 to $4.40Bn dollar range. The company also guided Q4 to about 61% YoY growth, above prior expectations. (Business Wire)

The stock popped after hours - I shorted in size at around $210. Fundamentals are great, I have no issue with the company. What matters is the price you are paying for them. Finviz and Yahoo show a forward P/E north of two hundred and a triple-digit price-to-sales ratio around the 130 to 140 range as of today, which puts Palantir in rarified air even within AI leaders.

When a stock trades at that altitude, it needs a clean chain of evidence: sequential pilot-to-production conversions, shrinking services intensity, and sustained GAAP margin expansion without financial engineering. Miss on any of those and multiple compression can do the work for you.

Competitive gravity

The world around Palantir has changed. In 2023, AIP demos looked singular because they fused governance, retrieval, tool-calling, and agentic behavior into operations when few production options existed.

In 2025, hyperscalers and data-platform incumbents have moved rapidly to bundle similar primitives inside estates customers already pay for. Microsoft put Agent Framework into public preview in October, unifying AutoGen and Semantic Kernel as an open-source SDK and runtime for multi-agent systems that plugs into Azure AI Studio and the fabric of Microsoft’s data estate.

Databricks ships the Mosaic AI Agent Framework tied to Unity Catalog governance and publishes step-by-step tutorials for building, evaluating, and deploying retrieval agents with notebook-level examples.

Snowflake’s Cortex suite keeps LLM-powered analysis and agentic behavior inside Snowflake with a governed semantic model, a REST API for Cortex Analyst, observability, and AISQL.

AWS Bedrock provides model choice and configurable guardrails, with documentation and APIs for building and applying safety and policy controls across foundations.

None of these is a one-for-one substitute for Gotham-class missions. They do narrow AIP’s perceived differentiation across median enterprise workloads, especially when paired with integrators and bundled into existing cloud or lakehouse commitments. That exerts price pressure and compresses the perceived “AI tax” unless Palantir can prove unique operational lift in each target domain. (Microsoft Azure)

The conversion gap

Palantir’s go-to-market engine has leaned heavily on workshops, trials, and pilots that show customers how agentic workflows feel against governed data. That is a rational wedge into conservative organizations. It is not, by itself, the cash engine.

The destination that matters is standardized, repeatable production apps with low services drag and durable net expansion.

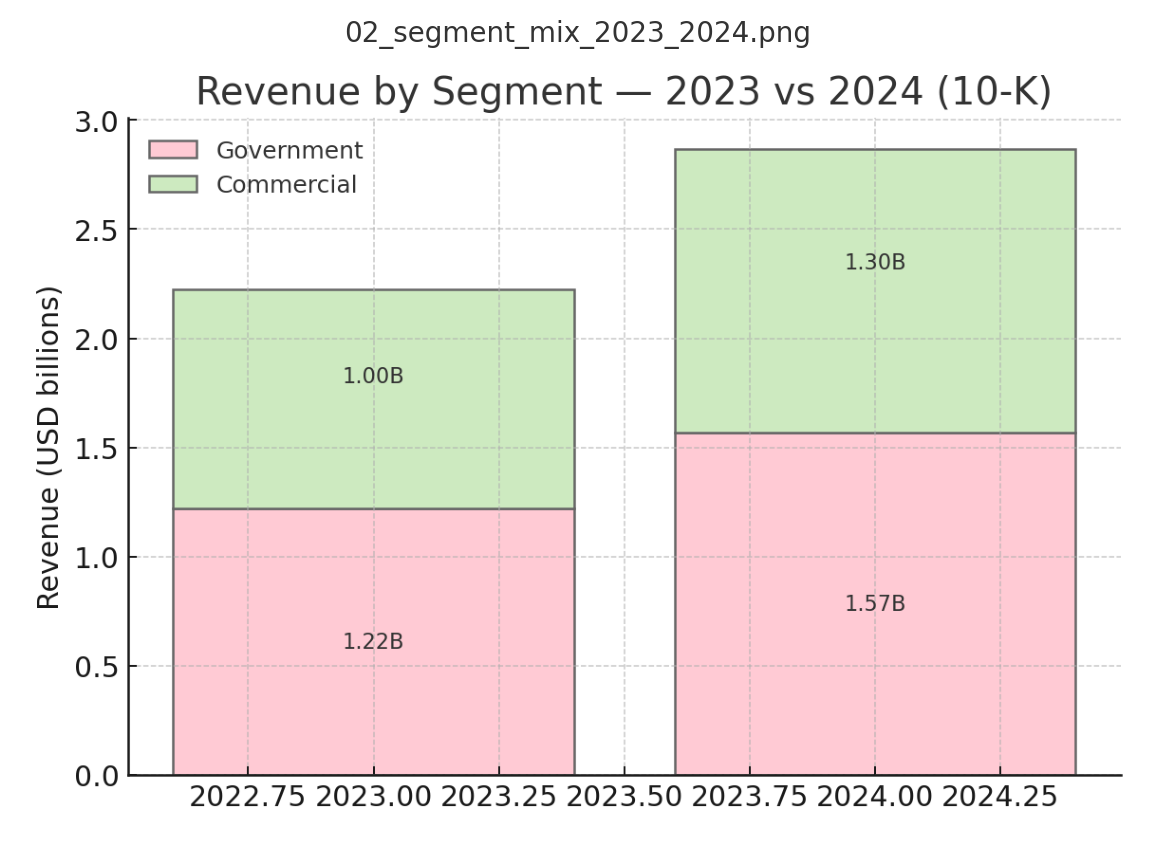

The company’s risk language stresses deal concentration, public-sector budget dynamics, and timing variance that can swing quarters. That concentration is a feature of serving critical agencies and a risk for a stock priced for inevitability. Breadth of logos needs to translate into templatized deployments that scale across business units with consistent margins.

Until your proof points shift decisively from bespoke shows of force to productized rollouts, the Street will debate how much of the pipeline is demos versus dollars. The filings make the lumpy reality clear; the market has preferred to see straight lines. (Palantir Investors)

Reasons to short

I will stop typing here and share some charts with you, the story is obvious.

What would change my mind

The short loses its edge if Palantir stacks several quarters where commercial pilot conversion accelerates and shows up as standardized, repeatable production deployments with diminishing services intensity, and if GAAP operating margin holds and expands into the mid-20s without one-time levers.

I would also look for dispersion to shrink: fewer single-deal cliffs, less concentration risk, and steady net expansion across a broader base.

If the stock crosses $250 psychological level, I don’t care about fundamentals I’d take the loss and get out.

Conclusion

Palantir is a real software vendor that built for domains other companies sidestepped and proved that governed AI can drive decisions where failure costs are high.

The short case says the stock already discounts a world where that edge turns into fast, horizontal adoption across the median enterprise at cloud-software velocity.

The product and the competition suggest a narrower, steadier path that still describes an excellent business but not the valuation in front of us.

The stock is overbought and is a good hedge going into the last two months of a momentous year for ADFM.